Value investors seeking the best stocks to buy may use a company’s 52-week low as a key metric to consider. Stock Rover’s screener provides a simple-to-use option for investors to find such stocks which have traded at those lows within the last 15 days. After running the initial stock screener, and answering the “who” question, investors should ask “why” next.

Stocks that are temporarily down on their luck tend to provide a greater chance of seeing above-average gains. However, such companies need to see marked improvements for such gains to be realized. Thus, whether these are beaten-down stocks to buy, or value traps to avoid, relies on what these companies do to fix their sometimes-broken business models.

Investors looking at these stocks need to critically assess the management teams which have driven poor results. Very often, the executives at such companies are overly optimistic. They will not say anything negative against the company. That’s because doing so may only hurt the stock price further.

InvestorPlace – Stock Market News, Stock Advice & Trading Tips

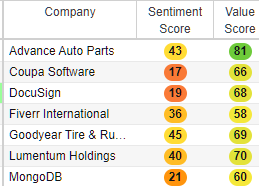

These stocks have low sentiment scores as investors ignore them.

The chart above lists stocks that traded at a 52-week low in the last 15 days. Additionally, each of these stocks trades at an average price above $4.00 a share. These companies could have issued a poor outlook, reported a weaker quarter, or simply trades at too high a valuation. In either case, each of these are stocks to buy for those looking for turnaround stories right now.

|

Advanced Auto Parts |

$147.69 |

|

|

Coupa Software |

$44.94 |

|

|

DocuSign |

$43.56 |

|

|

Fiverr |

$35.00 |

|

|

Goodyear Tire & Rubber |

$10.75 |

|

|

Lumentum Holdings |

$54.82 |

|

|

MongoDB |

$146.10 |

Advance Auto Parts (AAP)

Source: James R. Martin / Shutterstock

Let’s start our list of flattened stocks to buy with Advance Auto Parts (NYSE:AAP), a provider of after-market parts for the automotive sector. This company serves both do-it-yourself and professional customers.

Recently, AAP stock continued its decline, falling after disappointing third-quarter earnings. The company revenue of $2.6 billion, flat on a year-over-year basis. Management also lowered their revenue guidance for 2022, to the range of $11 billion to $11.2 billion.

Fearful investors anticipate a weaker economy will hurt auto parts sales. That said, I think these investors are missing out on the potential for shares to soar. In an internal deep dive, the company identified its underperformance in the Professional category. Advanced Auto Parts has the opportunity to move its inventory closer to the customer. This will improve product availability and will speed up its inventory turnover.

As the company spends more time with its suppliers to focus on key categories, I expect margins to expand. In 2023, Advanced Auto Parts will add more products that customers must have. This will increase sales volumes. In addition, in-house products will contribute positively to the company’s profitability.

Coupa Software (COUP)

Source: Shutterstock

Coupa Software (NASDAQ:COUP) provides a cloud platform for business spend management (“BSM”). While I think this is among the beaten-up stocks to buy, the market doesn’t agree. Coupa has been penalized due to broader economic worries around a potential recession on the horizon. Despite the prices of goods rising, customers must increase business spending in areas that matter. They will need Coupa’s solutions to manage those transactions.

Coupa needs to win back investor confidence. It must demonstrate to shareholders that the sales cycle is not elongated. Furthermore, I expect the company to refinance its convertible debt at favorable interest rates.

Coupa’s competitors do not have as strong a position in the mid-sized enterprise market. Additionally, I expect the company to manage a relatively weak sales cycle in Europe by engaging more closely with its customers. For example, Coupa may work more closely with European customers on transformation projects.

In North America, investors should expect Coupa’s strong scalable mid-market business to thrive. In this post-Covid environment, corporations may only see a minimal business slowdown. Thus, I expect many will renew their Coupa service contracts in 2023.

DocuSign (DOCU)

Source: Sundry Photography / Shutterstock.com

DocuSign (NASDAQ:DOCU) offers e-signature solutions for enterprise clientele. Notably, I think this is a company with many catalysts on the horizon.

One catalyst investors should watch is the potential for Docusing to increase the length of its client contracts. This is because the strong digitization trend allows for the acceleration of business processes (i.e. productivity increases) which will become much more valuable in a slowing economy.

Recently, DOCU stock bottomed at around $40. It now trades at a more reasonable price-to-sales ratio of 3.39 times. At this more attractive valuation, I think a larger software company that wants to strengthen its e-signature offerings might acquire DocuSign. Investors who hold shares at these levels will earn a high return on investment if that happens.

The economic slowdown will hurt some sectors more than others. Real estate transactions will fall as mortgage affordability falls. That will hurt DocuSign’s business in this sector. Conversely, the company will sharpen its focus on marketing its solution in other markets. Companies will value the reduced friction that their customers face through a digital signature process flow.

Fiverr International (FVRR)

Source: Temitiman / Shutterstock.com

Fiverr International (NYSE:FVRR) is a global online marketplace for freelance services. In the third quarter, Fiverr reported revenue growth of 11.0%, posting $82.5 million for its top line. For 2022, the company expects revenue of up to $340.0 million.

The company achieved higher sales per existing buyer by identifying an opportunity to increase active buyer spending in the quarter. Markets are stabilizing, but layoffs are picking up. For Fiverr, this could be a good thing, as more free agents on the market means more supply for the company. Thus, the economy’s loss could be Fiverr’s gain.

Additionally, customers searching for specific freelance services will increase. As demand rises, Fiverr’s revenue and operating profits are likely to strengthen. Historically, a short-term slowdown benefited its business. For example, during the Covid lockdown, supply increased, and as corporations rushed to invest in services, demand rose accordingly.

I think Fiverr’s business model remain in high demand in the year ahead. This is a company that is well-positioned to help its customers find staff that may perform more complicated, larger projects. Accordingly, the attractiveness of Fiverr’s marketplace for corporate customers will only get more attractive from here.

Goodyear Tire & Rubber (GT)

Source: Roman Tiraspolsky / Shutterstock.com

Investors have been in selling mode with Goodyear Tire & Rubber (NASDAQ:GT) after the company posted its third-quarter results. The tire supplier posted revenue of $5.31 billion, but showed weakness during the quarter. This was mainly due to two headwinds – increased inventory and stronger competition.

Goodyear also had higher raw material and energy costs. Thus, the company was unable to pass all inflationary pressures onto customers. In addition, labor costs rose. In North America, the company could potentially offset such costs. However, at a total company level, those factors eroded its profitability.

In the automotive marketplace, Goodyear performed well in the light truck market, in addition to strong performance in other key segments. However, the company has factories that operate in higher-cost locations compared to its competitors. Thus, this cost disadvantage is notable, as Goodyear’s customers are more sensitive to higher prices as their disposable income falls.

That said, I think GT stock has a good chance of rebounding quickly. The company has eliminated its excess capacity in the quarter, improving its competitive position by leveraging its production outside of Europe.

Lumentum Holdings (LITE)

Source: John-Fs-Pic / Shutterstock.com

Lumentum Holdings (NASDAQ:LITE) manufactures optical and photonic products. Like other names on this list, LITE stock fell when it posted its fiscal second-quarter results. While revenue grew by 13.0% to $506.8 million, its outlook for the current quarter came in weaker than expected. For the full year, the company expects non-GAAP diluted earnings per share of $1.20 to $1.45.

Ongoing supply shortages had the biggest impact on its results. This will likely continue into its fiscal 2024 year. Accordingly, investors who accumulate shares at a discount should expect a rally after the shortage ends. In addition, weaker sales of 3D sensing solutions from hyperscaler customers are temporary. Once demand rebounds, Lumentum will raise its outlook.

In the company’s telecom sector, I expect demand to remain strong. Additionally, Lumentum’s commercial lasers business should continue to thrive. Lumentum will thus have to play catch up to fulfill demand.

In its data center business, Lumentum has seen weaker demand affect inventories. That said, once chip supplies come into equilibrium, higher orders in the quarters to come should help the company raise its outlook, boosting its valuation.

MongoDB (MDB)

Source: Shutterstock

Last on our list of stocks to buy is database software provider MongoDB (NASDAQ:MDB). The company continues to offer agile solutions and real-time analytics. I expect customers to sustain their investments in technology that gives them an edge.

MongoDB is trading at a discount because its growth is slowing. Revenue growth could slow to the high teens in the fourth quarter, compared to a 55% growth rate in the first half of the year. However, the company’s MongoDB Atlas product has the potential to sustain growth of nearly 75%. In addition, its Enterprise Advanced product lets customers run MongoDB on their own. Customers who need security and efficiency may allocate their technology budget here.

Investors should bet on MongoDB winning new customers in the medium- to long-term. The company is in the very early stages of growing its market share. Thus, I think its share price will rise alongside increases in new customers in the coming quarters through its direct sales channel.

The weakening macroeconomic environment will encourage organizations to build applications with fewer resources. MongoDB offers the best way to do more with less.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get actionable insight to achieve strong investment returns.

More From InvestorPlace

The post 7 Stocks Ready to Soar After Flattening at Lows appeared first on InvestorPlace.