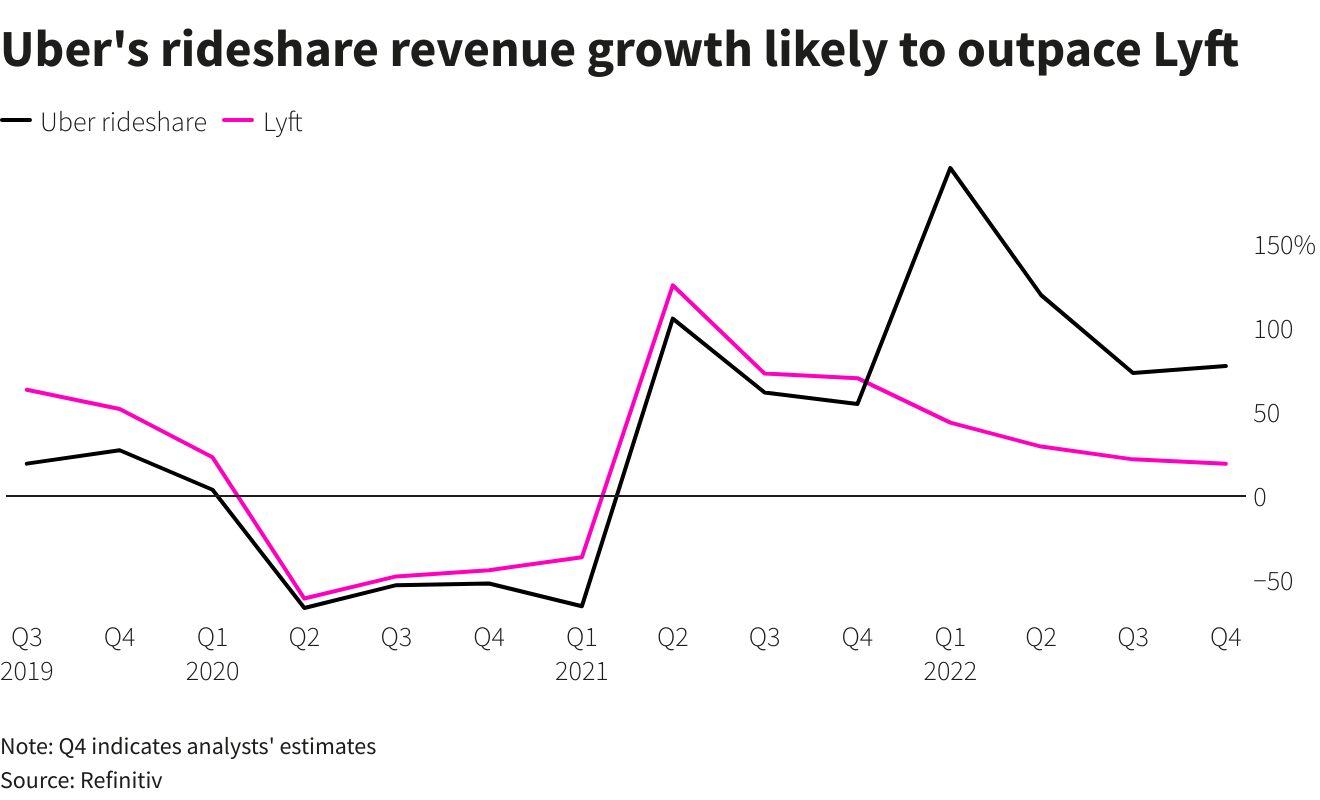

Feb 7 (Reuters) – Uber Technologies Inc’s (UBER.N) revenue growth is set to outpace that of rival Lyft Inc (LYFT.O) as the rideshare firm’s presence in major markets around the world gives it the heft to deal with inflationary pressures.

Ridesharing companies are starting to recover from pandemic lows as offices reopen and following a resurgence in travel on the back of reopening of closed borders and a strong U.S. dollar.

Dara Khosrowshahi-led Uber operates in multiple regions and has over the years built a massive food and grocery delivery business, while Lyft has mainly focused on rideshare in the United States.

Uber’s larger scale, reflected in a $67 billion market cap that is nearly ten times that of its rival, has also allowed it to spend more on incentives to attract drivers at a time when the industry recovery has flooded rideshare firms with demand.

Latest Updates

View 2 more stories

While Lyft was the first to show glimpses of a profit since rideshare operations began, investors will now focus on adjusted core earnings outlook as the companies have set big targets for 2024 – $5 billion by Uber and $1 billion by Lyft.

“Lyft is on the losing end of Uber’s mobility and delivery network effect … in a world of increasing focus on profitability, Lyft does not deliver,” MoffettNathanson analyst Michael Morton said.

Analysts expect a fourth-quarter revenue increase of 19% for Lyft and 47% for Uber, according to Refinitiv data.

CONTEXT

Analysts at UBS pointed to data that showed the time drivers spent on the Lyft app had decreased, while share of driver app downloads increased for Uber in the fourth quarter.

“When we look at driver time spent data on a 2-year growth basis our concerns on Lyft losing market share are magnified … we come away more concerned about Lyft’s need to invest in incentives,” UBS analyst Lloyd Walmsley said.

Uber’s food and delivery segment, which makes up for more than a third of its revenue, has so far been resilient in the weakening economy but it faces risks from a pullback in consumer spending.

FUNDAMENTALS

** Analysts expect Uber to report fourth-quarter adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) of $614.79 million and an adjusted loss of 18 cents per share

** Lyft is likely to report adjusted EBITDA of $91 million, an increase of 22%, and adjusted earnings of 13 cents per share

WALL STREET SENTIMENT

** Fourteen of 47 analysts rate Uber “strong buy”, 28 “buy” and five “hold”

** Five of 46 analysts covering Lyft have a “strong buy” rating, 16 “buy”, 24 “hold” and one “sell”

Reporting by Nivedita Balu in Bengaluru; Editing by Shounak Dasgupta

Our Standards: The Thomson Reuters Trust Principles.