Feb 28 (Reuters) – Satoshi Nakamoto would be proud. Adolescent bitcoin may finally be repaying its creator’s faith.

The 15-year-old cryptocurrency has filled many roles – from source of speculation to hedge against inflation – but has struggled to find a clear identity. Now there are growing signs it’s edging towards its intended purpose: payments.

“The development in terms of building out crypto payments has continued apace, even if it’s gone somewhat unnoticed because of the volatility in the broader market,” said Richard Mico, U.S. CEO of Banxa, a payment-and-compliance infrastructure provider.

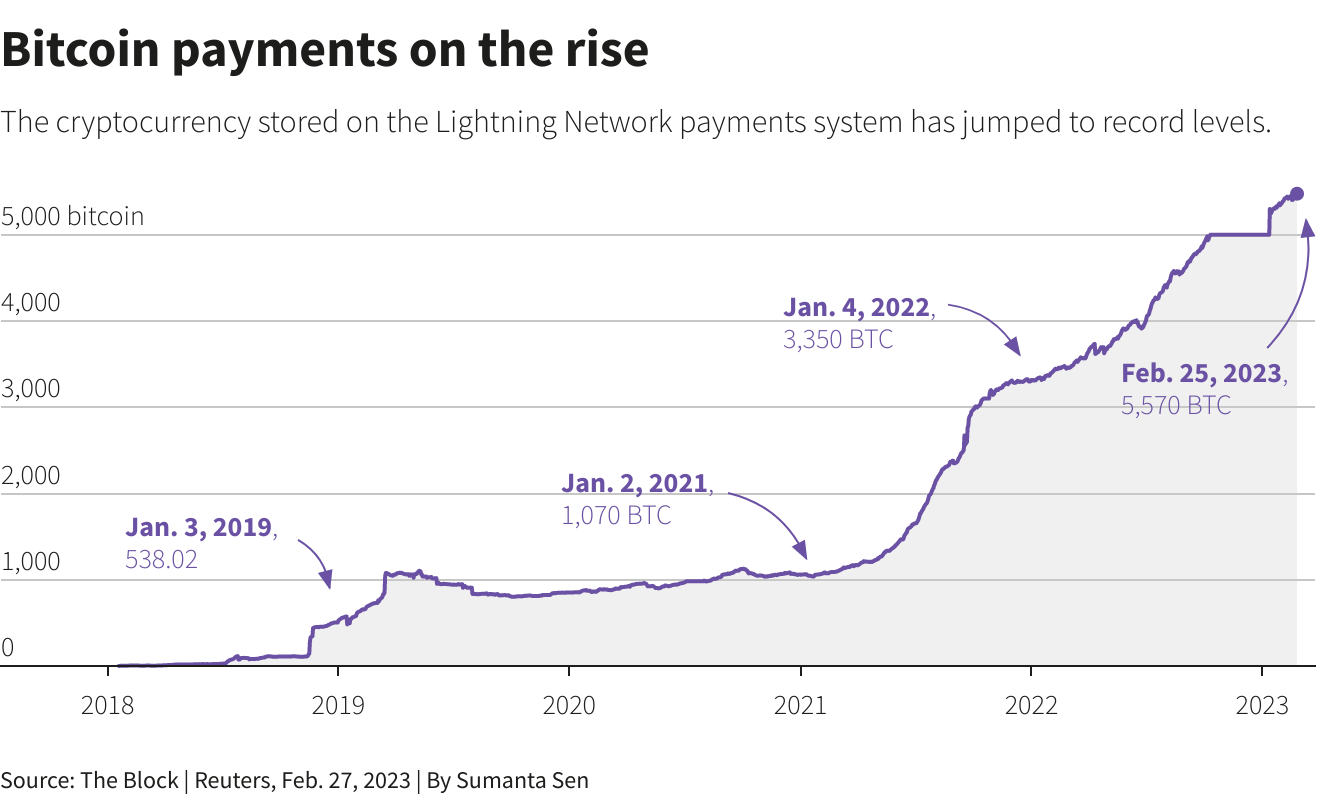

The amount of bitcoin stored on the Lightning Network – a payment protocol layered on top of the blockchain – has jumped by two-thirds over the past year to hit an all-time high of 5,580 coin, according to crypto data firm The Block.

Crypto payment specialists have also seen strong volumes.

U.S.-based BitPay said transaction volumes jumped 18% last year versus 2021. CoinsPaid said volumes in the fourth quarter of 2022 rose 32% compared with a year before.

Latest Updates

View 2 more stories

BITCOIN AND BRAZILIAN REAL

So why has crypto failed to fulfill pseudonymous inventor Nakamoto’s dream, spelt out in a famed 2008 white paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System”?

Price volatility, slow processing speeds and persistent regulatory uncertainty are among the factors that have rendered cryptocurrencies unwieldy as a means of payment. Few merchants price good or services in crypto.

Nonetheless, proponents say bitcoin offers lower transaction costs and quicker speeds than traditional cash, especially for cross-border transfers.

Aside from bitcoin, other cryptocurrencies including stablecoins, which are pegged to the value of traditional currencies, have emerged as popular options, particularly for cross-border payments, remittances, plus in emerging markets where the value of local currencies have been hit by inflation.

Stellar, a blockchain that enables cross-border payments, saw the number of trades on its platform increase to 103.4 million last month from 50.6 million in January 2022.

Volumes for trades across exchanges between bitcoin and Turkey’s lira and Brazil’s real increased by 232% and 72%, respectively, CryptoCompare data showed.

CAN YOU HANDLE THE STRESS?

It’s not all smooth sailing for the widespread adoption of crypto for payments; for one thing, there’s the question of whether blockchains are ready to handle the stress of processing thousands of transactions at a time, especially without a simultaneous jump in transaction fees.

Efforts by some of the world’s largest economies, including Japan, China and India, to create their own digital currencies (CBDCs) could also choke crypto payments growth, say some market players. For others, though, growing interest in CBDCs is evidence that blockchain payments tech is here to stay.

Traditional finance firms looking to embrace crypto payments have also shrugged off recent market volatility. One, Visa (V.N) inking a deal this month with crypto firm WireX to directly issue crypto-enabled debit and prepaid cards.

“Crypto is evolving into a viable alternative for more and more people around the world,” said Mico at Banxa.

Reporting by Lisa Pauline Mattackal and Medha Singh in Bengaluru; Editing by Tom Wilson and Pravin Char

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.