March 8 (Reuters) – The once high-flying fintech startups looking to go public will have a hard time attracting investor attention, even though a freeze that has gripped the market for new listings is starting to thaw.

Activities related to initial public offerings (IPO) in the United States came to a standstill for more than a year as the U.S. Federal Reserve’s aggressive monetary-tightening policy sucked out easy money from the system.

The cautious mood in the market has meant that mostly those startups that are backed by solid fundamentals and steady revenue streams have dared to go public, with roughly 24 companies listing their shares this year and about 140 filing for IPOs.

As investor confidence improves, more companies are expected to reignite their IPO plans this year, but fintech firms may opt out of the race as they face a string of worries, including rising cash-burn rate, mounting losses and poor share performance of some of their listed peers.

Latest Updates

View 2 more stories

“We’re still in the early innings of the IPO market’s pick-up. And when IPO activity does resume, we expect fintechs will likely be among the last to rejoin the party,” said Matthew Kennedy, senior strategist at IPO research firm Renaissance Capital.

“I don’t think it would surprise anyone if they all sat out the 2023 IPO market,” Kennedy added.

Digital banking pioneers Chime and Stripe are currently seen as the industry’s top IPO candidates along with investing app Acorns and buy-now-pay-later firm Klarna.

BOOM AND BUST

Fintech apps soared in popularity during the COVID-19 pandemic, as a near-zero interest rate environment helped them offer easy credit to lure consumers who were stuck at home.

Digital payments giants like PayPal Holdings Inc (PYPL.O) and Block Inc (SQ.N) also expanded their buy now, pay later (BNPL) services to appeal to millennials and Gen Z customers.

But with interest rates at their highest levels since the global financial crisis, apps with huge exposure to subprime borrowers have attracted investor scrutiny, making it tough for such startups to justify higher valuations.

“On the fintech side, it is not one-size-fits-all. Fintechs that have maintained their growth and market share focus may not play well into the current market focus on profitability,” said Rachel Gerring, EY Americas IPO leader, and Mark Schwartz, IPO and SPAC Capital Markets Advisory leader.

They, however, said there were companies in the sector with the scale and cash flow for whom individual circumstances would determine whether to push forward with their IPO plans or opt for a wait-and-see approach.

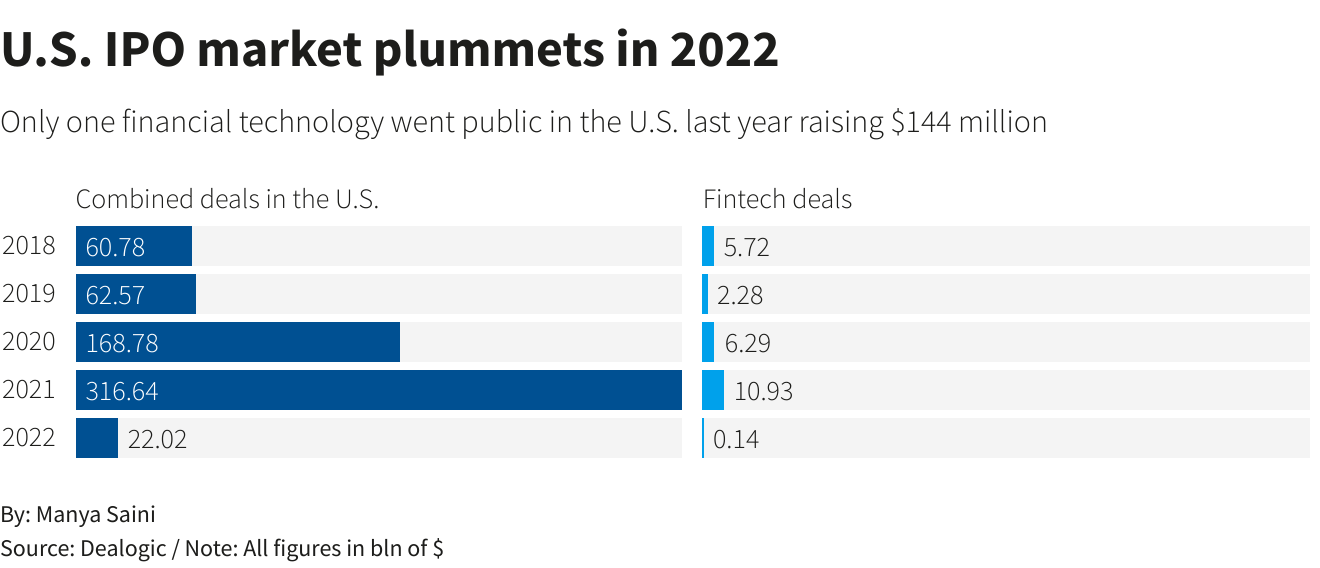

In the IPO boom of 2021, 20 fintech companies raised a combined $10.93 billion, vastly overshadowing the $144 million that was raised by a lone offering in the following year, according to data from Dealogic.

“The IPO market is not closed, but it’s certainly more valuation and profitability focused,” said David Ethridge, U.S. co-IPO leader at global consulting giant PwC.

Companies looking to list will need to shore up investor confidence in their cost-cutting plans and be transparent with their attempts to lower cash burn, he added.

LACKLUSTRE LISTINGS

Listed fintech companies have failed to largely live up to their shareholders’ expectations as they have steadily booked losses, leading to a string of routs in their shares.

Coinbase, which was valued at $86 billion in its Nasdaq debut in April 2021, now has a market capitalization of about $15 billion.

Robinhood and BNPL lender Affirm Holdings (AFRM.O) have shed $20 billion each in valuations since going public.

High-growth fintechs were previously valued like tech companies, where valuation was decided as a multiple of sales. But with the tech boom having subsided, they are being evaluated using the playbook investors use for financial firms, where earnings play a crucial role, Renaissance’s Kennedy said.

Reporting by Manya Saini in Bengaluru; Editing by Anil D’Silva

Our Standards: The Thomson Reuters Trust Principles.