While some trends from 2023 may disappear, one that likely won’t is the growing percentage of the global automobile fleet converting to electric vehicles (EVs). In the U.S., less than 10% of total automobile sales are now EVs. In China, that percentage is higher, with battery electric vehicles (BEVs) accounting for 25% of new sales in September 2023.

This makes China a critical EV market for investors, and Nio (NIO -2.55%) is a company that often comes up when researching Chinese EV companies. With EVs slated to capture even more market share in 2024, is Nio a good buy right now?

Nio is not China’s largest EV producer

Although Nio is a popular Chinese EV investment for U.S. investors, it’s far from China’s biggest EV maker. That title belongs to BYD (BYDDY 0.41%). In December, Nio delivered over 18,000 vehicles, up 14% year over year. For 2023, it delivered over 160,000 vehicles, up 31%.

In comparison, BYD produced over 3 million cars in 2023 and nearly 309,000 in December alone. So size-wise, Nio isn’t even close to BYD.

But the two are serving different markets. Nio is focused on the luxury segment, while BYD offers more affordable EVs. As a result, Nio will likely never reach the same scale as BYD, but that doesn’t disqualify Nio as a potential investment.

However, it should be noted that China’s economy isn’t doing particularly well. This could spell trouble for Nio if drivers look to cheaper options instead of more premium ones. While it remains to be seen if this will have an effect in 2024, it’s something to consider before taking a position in Nio.

Another consideration is its financials.

Nio is unprofitable and burning cash quickly

Nio is a rapidly growing company. In the third quarter, its sales rose 46% year over year to RMB17.4 billion. However, it isn’t profitable. Nio lost RMB4.8 billion ($658 million) from operations, which isn’t far from breaking even. With RMB5.3 billion in cash on hand ($726 million), Nio is also in danger of running out of money.

However, in mid-December 2023, Nio announced a $2.2 billion investment from U.S. investment firm CYVN. This will shore up Nio’s finances momentarily, but the company is in a race with the clock to become profitable.

The fourth quarter also isn’t looking the greatest. Nio only projected to deliver between 47,000 and 49,000 vehicles, yet exceeded expectations by delivering over 50,000. However, thanks to price cuts, Nio’s revenue was only supposed to grow by about 4% on the high end. While the delivery beat may increase its growth rate, growing revenue in the mid-single digits isn’t a great recipe for a company trying to break even.

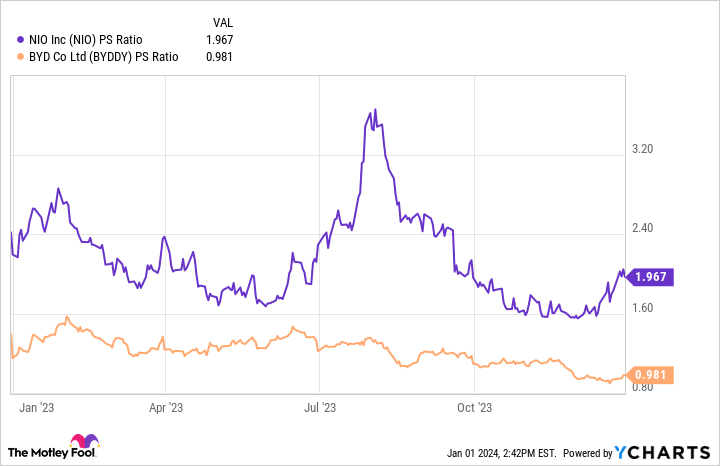

Despite that, Nio trades at a premium to established China EV player BYD.

NIO PS Ratio data by YCharts

Considering that BYD grew its Q3 revenue at nearly 40%, purchasing Nio instead of BYD doesn’t seem like a smart investment move.

There’s a reason why smart investment firms like Berkshire Hathaway own BYD stock, not Nio (Berkshire owns 8% of BYD). Investing in China is already hard enough; investors don’t need to add more difficulty by investing in upstarts in a highly competitive industry.

While Nio may have a great product, the stock doesn’t seem worth the risk.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends BYD and Nio. The Motley Fool has a disclosure policy.