Amidst a backdrop of global economic fluctuations and specific challenges within the Hong Kong market, investors are keenly observing trends and potential opportunities. High insider ownership in growth companies on the SEHK can signal strong confidence from those who know these businesses best, making such stocks particularly interesting in these uncertain times.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

iDreamSky Technology Holdings (SEHK:1119) |

20.1% |

104.1% |

|

New Horizon Health (SEHK:6606) |

16.6% |

62.3% |

|

Fenbi (SEHK:2469) |

32.1% |

43% |

|

Meitu (SEHK:1357) |

38% |

33.7% |

|

DPC Dash (SEHK:1405) |

38.2% |

89.7% |

|

Adicon Holdings (SEHK:9860) |

22.3% |

29.6% |

|

Zylox-Tonbridge Medical Technology (SEHK:2190) |

18.5% |

79.3% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

100.1% |

|

Beijing Airdoc Technology (SEHK:2251) |

27.9% |

83.9% |

|

Ocumension Therapeutics (SEHK:1477) |

17.7% |

93.7% |

We’ll examine a selection from our screener results.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited operates in the automobile and battery sectors across China, Hong Kong, Macau, Taiwan, and internationally, with a market capitalization of approximately HK$715.83 billion.

Operations: The company’s revenue is derived from its automobile and battery sectors across various regions including China, Hong Kong, Macau, Taiwan, and internationally.

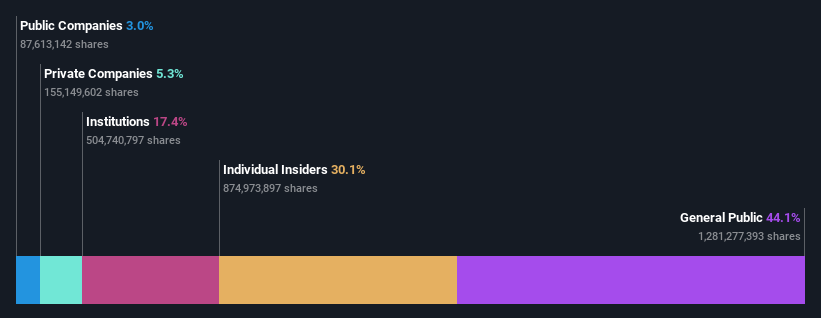

Insider Ownership: 30.1%

Return On Equity Forecast: 22% (2027 estimate)

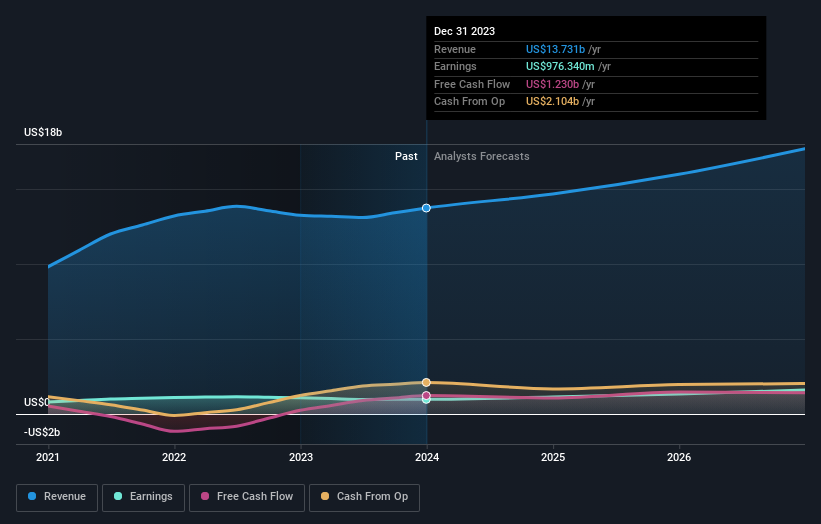

BYD, a prominent player in Hong Kong’s growth sectors with substantial insider ownership, is navigating a competitive landscape. Its revenue and earnings are projected to outpace the broader Hong Kong market with annual increases of 14.5% and 14.7%, respectively. Despite this robust growth, its performance isn’t classified as significantly high since it falls below the 20% threshold for notable earnings expansion. Additionally, BYD’s Return on Equity is expected to be strong at 22.2%. The company recently declared an increased dividend payout and reported significant sales and production volume increases year-over-year, signaling operational strength amid expanding market presence.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Meituan is a technology retail company based in the People’s Republic of China, with a market capitalization of approximately HK$698.33 billion.

Operations: The company generates revenue primarily through Core Local Commerce and New Initiatives, with segments totaling CN¥206.91 billion and CN¥69.84 billion respectively.

Insider Ownership: 12.2%

Return On Equity Forecast: 21% (2026 estimate)

Meituan, a growth-oriented company with significant insider ownership in Hong Kong, is trading at 64.9% below its estimated fair value. Its earnings are expected to grow by 33.16% annually over the next three years, outpacing the Hong Kong market’s forecasted growth. The company has recently turned profitable with substantial year-over-year revenue and net income increases reported in Q1 2024. Insider activities show more buying than selling in recent months, underscoring confidence from within despite a lack of substantial purchases recently.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Techtronic Industries Company Limited, with a market capitalization of HK$182.99 billion, is involved in designing, manufacturing, and marketing power tools, outdoor power equipment, and floorcare and cleaning products across North America, Europe, and other global markets.

Operations: Techtronic Industries generates revenue primarily through two segments, with power equipment contributing $12.79 billion and floorcare & cleaning products adding $0.97 billion.

Insider Ownership: 25.3%

Return On Equity Forecast: 21% (2026 estimate)

Techtronic Industries, recognized for its robust insider ownership, is navigating a period of transition and growth. With the recent CEO change to Steven Richman, who brings extensive industry experience, the company remains poised for progress. It recently initiated a significant share repurchase program aimed at enhancing shareholder value. Despite a slight dip in net income from the previous year, Techtronic’s earnings are projected to grow 15.87% annually, slightly outpacing broader market expectations in Hong Kong.

Turning Ideas Into Actions

Curious About Other Options?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1211 SEHK:3690 and SEHK:669.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com