Amidst a backdrop of fluctuating global markets, the Hong Kong stock exchange continues to present intriguing opportunities for investors. High insider ownership in growth companies is often seen as a positive indicator of confidence in the company’s future prospects, aligning closely with current market trends that favor technology and growth-oriented sectors.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

iDreamSky Technology Holdings (SEHK:1119) |

20.1% |

104.1% |

|

Fenbi (SEHK:2469) |

32.4% |

43% |

|

Zylox-Tonbridge Medical Technology (SEHK:2190) |

18.5% |

79.3% |

|

Adicon Holdings (SEHK:9860) |

22.3% |

29.6% |

|

Tian Tu Capital (SEHK:1973) |

34% |

70.5% |

|

DPC Dash (SEHK:1405) |

38.2% |

89.7% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

100.1% |

|

Zhejiang Leapmotor Technology (SEHK:9863) |

15% |

76.5% |

|

Beijing Airdoc Technology (SEHK:2251) |

28.2% |

83.9% |

|

Lianlian DigiTech (SEHK:2598) |

19.4% |

84.2% |

Let’s dive into some prime choices out of from the screener.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited operates in the automobile and battery sectors across China, including Hong Kong, Macau, Taiwan, and internationally, with a market capitalization of approximately HK$754.99 billion.

Operations: The company’s revenue is generated primarily from its automobile and battery sectors.

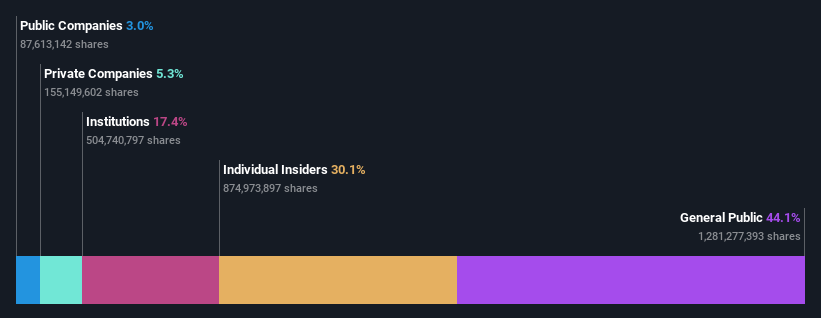

Insider Ownership: 30.1%

Earnings Growth Forecast: 14.8% p.a.

BYD, a prominent growth company in Hong Kong with high insider ownership, has demonstrated robust performance with a 52.7% increase in earnings over the past year. Despite this strong growth, forecasts suggest more moderate future expansions, with expected annual revenue and profit growth rates at 14% and 14.8%, respectively—both figures surpassing local market averages but not reaching significantly high levels. The company’s strategic moves include amending its bylaws and consistently increasing dividends, indicating stable governance and shareholder value focus. Recent sales data show significant volume increases year-over-year, reinforcing its market position amidst expanding operations like the launch of BYD SHARK in Mexico.

Simply Wall St Growth Rating: ★★★★☆☆

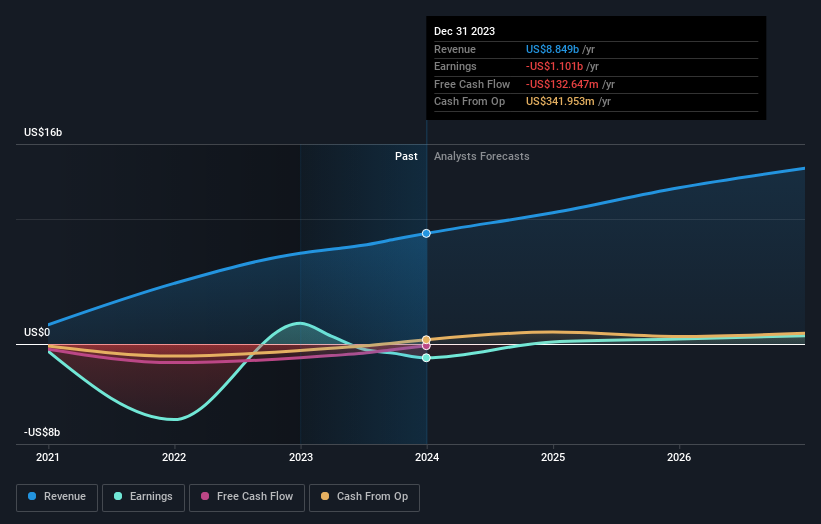

Overview: J&T Global Express Limited, primarily an investment holding company, provides express delivery services and has a market capitalization of approximately HK$77.11 billion.

Operations: The company generates revenue primarily from its air freight transportation segment, totaling HK$8.85 billion.

Insider Ownership: 20.2%

Earnings Growth Forecast: 102.9% p.a.

J&T Global Express, a growth-oriented firm in Hong Kong with significant insider ownership, has seen substantial revenue growth of 21.8% over the past year. Despite a forecasted modest return on equity at 17.9%, the company’s earnings are expected to surge by 102.86% annually. This performance is particularly notable as J&T’s revenue growth rate of 15.9% per year outpaces the local market average of 7.8%. Recent board changes and strong parcel volume underline its dynamic operational environment and strategic adaptability.

Simply Wall St Growth Rating: ★★★★★☆

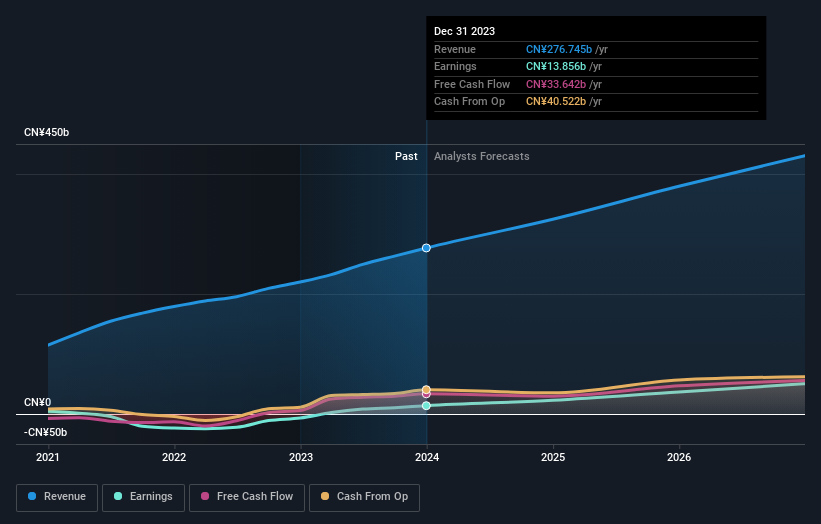

Overview: Meituan is a technology retail company based in the People’s Republic of China, with a market capitalization of approximately HK$751.32 billion.

Operations: The company generates revenue through technology retail operations in China.

Insider Ownership: 11.4%

Earnings Growth Forecast: 31.5% p.a.

Meituan, a company with high insider ownership, demonstrates robust growth potential in Hong Kong. Its revenue is expected to increase by 12.7% annually, outpacing the local market’s 7.8%. Notably, earnings have surged by a very large percent over the past year and are projected to grow at 31.5% per year. Recent financials show a significant rise in quarterly sales to CNY 73.28 billion and net income to CNY 5.37 billion, reflecting strong operational performance despite substantial one-off items impacting results.

Next Steps

Interested In Other Possibilities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1211 SEHK:1519 and SEHK:3690.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com