Amid a backdrop of mixed global economic signals, the Hong Kong market has shown resilience with the Hang Seng Index marking a modest gain in a holiday-shortened week. In such an environment, growth companies with high insider ownership in Hong Kong can be particularly compelling as these firms often benefit from aligned interests between shareholders and management, fostering robust long-term strategies even in uncertain times.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

iDreamSky Technology Holdings (SEHK:1119) |

20.2% |

104.1% |

|

Pacific Textiles Holdings (SEHK:1382) |

11.2% |

37.7% |

|

Fenbi (SEHK:2469) |

32.8% |

43% |

|

Tian Tu Capital (SEHK:1973) |

34% |

70.5% |

|

Adicon Holdings (SEHK:9860) |

22.4% |

28.3% |

|

Zhejiang Leapmotor Technology (SEHK:9863) |

15% |

73.4% |

|

DPC Dash (SEHK:1405) |

38.2% |

90.2% |

|

Beijing Airdoc Technology (SEHK:2251) |

28.7% |

83.9% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

100.1% |

|

Ocumension Therapeutics (SEHK:1477) |

23.1% |

93.7% |

Let’s dive into some prime choices out of from the screener.

Simply Wall St Growth Rating: ★★★★★☆

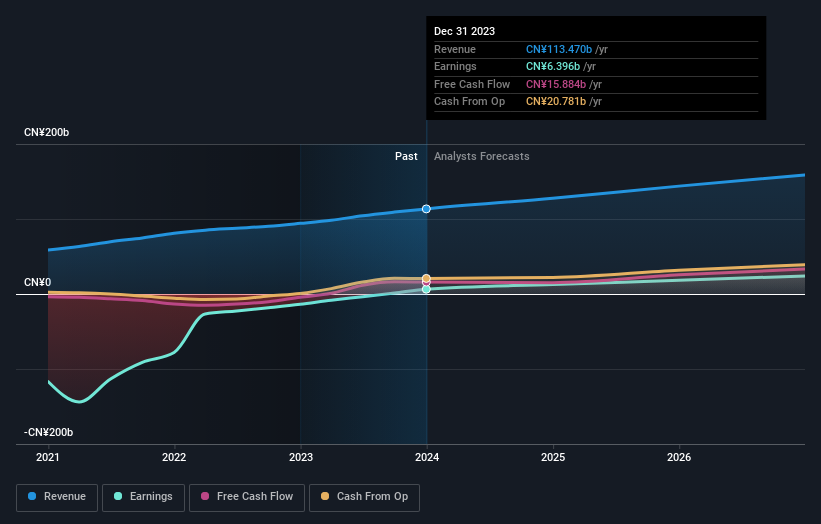

Overview: Kuaishou Technology operates as an investment holding company in the People’s Republic of China, offering services such as live streaming and online marketing, with a market capitalization of approximately HK$207.67 billion.

Operations: The company generates revenue primarily through domestic operations, which amounted to CN¥114.72 billion, and a smaller portion from overseas activities totaling CN¥2.94 billion.

Insider Ownership: 19.2%

Earnings Growth Forecast: 22.5% p.a.

Kuaishou Technology, a notable growth company in Hong Kong with significant insider ownership, has recently demonstrated robust advancements in AI technology, enhancing its commercial ecosystem. At the 2024 World Artificial Intelligence Conference, the company unveiled upgrades to its AI models such as Kling and Kolors, boosting user engagement and commercial applications. Financially, Kuaishou reported a substantial turnaround with Q1 earnings of CNY 4.12 billion in 2024 from a loss the previous year and is executing a share buyback program worth HK$16 billion valid until 2027. Despite trading below analyst price targets and perceived fair value, expectations for revenue growth are optimistic relative to the market.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited operates in the automobile and battery sectors across China, Hong Kong, Macau, Taiwan, and internationally with a market capitalization of approximately HK$755.62 billion.

Operations: The company’s revenue is primarily derived from its automobile and battery segments across various regions including China, Hong Kong, Macau, and Taiwan.

Insider Ownership: 30.1%

Earnings Growth Forecast: 15.3% p.a.

BYD, a growth-oriented company in Hong Kong with high insider ownership, has shown impressive performance with strong sales and production increases year-over-year as of June 2024. Despite trading at 47% below estimated fair value, BYD’s revenue is expected to grow faster than the Hong Kong market average. Earnings are also projected to expand annually by 15.29%. The company recently enhanced its product line with the launch of BYD SHARK in Mexico, marking its first global product introduction outside China and underscoring its innovation capabilities and expansion strategy. However, it should be noted that earnings growth is not considered significantly high compared to industry benchmarks.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ESR Group Limited operates in logistics real estate development, leasing, and management across regions including Hong Kong, China, Japan, South Korea, Australia, New Zealand, Southeast Asia, India, and Europe with a market capitalization of approximately HK$50.56 billion.

Operations: The company generates revenue primarily through fund management at HK$774.64 million and new economy development at HK$105.48 million.

Insider Ownership: 13.1%

Earnings Growth Forecast: 26.5% p.a.

ESR Group, a key entity in Hong Kong’s growth sector with substantial insider ownership, is navigating a complex landscape. Despite trading 36.6% below its fair value and facing challenges like low forecasted Return on Equity at 7.3%, ESR’s earnings are expected to surge by 26.5% annually, outpacing the local market’s growth. Recent strategic moves include potential privatization discussions led by significant shareholders and consortiums, reflecting a dynamic shift in its operational focus and ownership structure amidst fluctuating market conditions.

Key Takeaways

Seeking Other Investments?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1024 SEHK:1211 and SEHK:1821.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com