As Hong Kong’s Hang Seng Index shows signs of resilience with a 1.99% gain, investors are increasingly looking for growth opportunities in the region. One key indicator of a promising stock is high insider ownership, which often signals confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

iDreamSky Technology Holdings (SEHK:1119) |

18.8% |

104.1% |

|

Pacific Textiles Holdings (SEHK:1382) |

11.2% |

37.7% |

|

Adicon Holdings (SEHK:9860) |

22.4% |

28.3% |

|

Zhejiang Leapmotor Technology (SEHK:9863) |

15% |

76.4% |

|

Zylox-Tonbridge Medical Technology (SEHK:2190) |

18.7% |

79.3% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

100.1% |

|

Value Partners Group (SEHK:806) |

23.4% |

59.5% |

|

Beijing Airdoc Technology (SEHK:2251) |

28.6% |

83.9% |

|

Beijing Fourth Paradigm Technology (SEHK:6682) |

22.8% |

104.2% |

|

DPC Dash (SEHK:1405) |

38.2% |

91.5% |

Let’s review some notable picks from our screened stocks.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited, with a market cap of HK$712.82 billion, operates in the automobiles and batteries business across China, Hong Kong, Macau, Taiwan, and internationally.

Operations: The company’s revenue segments include automobiles and batteries, serving markets in China, Hong Kong, Macau, Taiwan, and internationally.

Insider Ownership: 30.1%

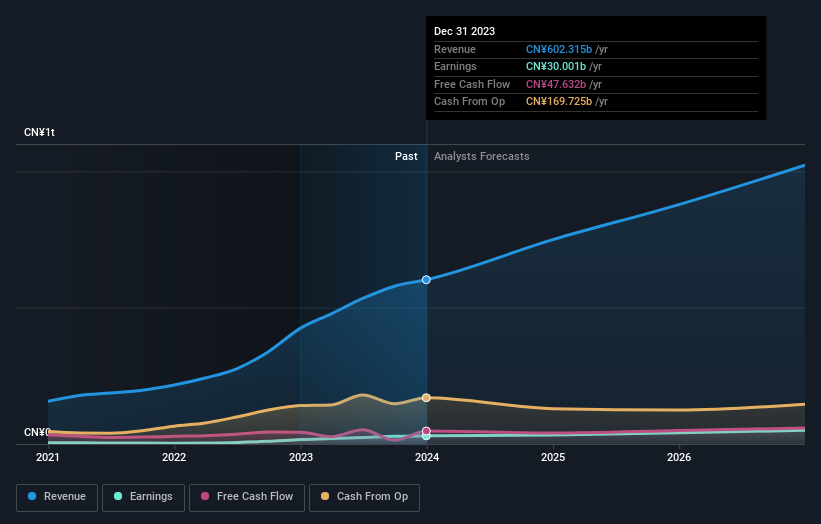

BYD has shown robust growth with a 52.7% increase in earnings over the past year and is forecasted to grow its revenue by 14% annually, outpacing the Hong Kong market. Recent strategic partnerships, such as with Uber for deploying 100,000 electric vehicles globally, bolster its expansion efforts. High insider ownership aligns management’s interests with shareholders, while recent production and sales volumes indicate strong operational performance.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Meituan is a technology retail company in the People’s Republic of China with a market cap of HK$661.07 billion.

Operations: The company’s revenue segments are: Food Delivery (CN¥96.29 billion), In-Store, Hotel & Travel (CN¥32.45 billion), and New Initiatives & Others (CN¥59.74 billion).

Insider Ownership: 11.6%

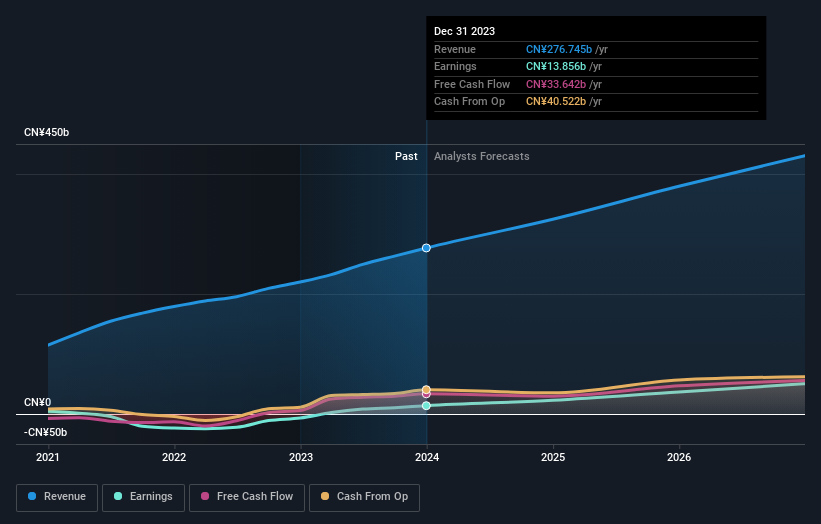

Meituan’s earnings surged by 568.2% last year and are expected to grow at 31.3% annually, surpassing the Hong Kong market average. The company recently announced a $2 billion share repurchase program, reflecting confidence in its future prospects despite no substantial insider buying in the past three months. Recent changes in company bylaws and board composition may also impact governance and strategic direction positively.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Techtronic Industries Company Limited designs, manufactures, and markets power tools, outdoor power equipment, and floorcare and cleaning products across North America, Europe, and internationally with a market cap of HK$189.30 billion.

Operations: The company generates revenue primarily from Power Equipment, which accounts for $13.23 billion, and Floorcare & Cleaning products, contributing $965.09 million.

Insider Ownership: 25.4%

Techtronic Industries reported half-year sales of US$7.31 billion, up from US$6.88 billion a year ago, with net income rising to US$550.37 million from US$475.78 million. The company announced an interim dividend of HKD 1.08 per share and appointed Steven Richman as Executive Director, reflecting strong internal leadership and growth potential. Insider buying has been substantial recently, indicating confidence in the company’s future performance amidst steady revenue and earnings growth forecasts above market averages.

Seize The Opportunity

Ready For A Different Approach?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1211 SEHK:3690 and SEHK:669.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com