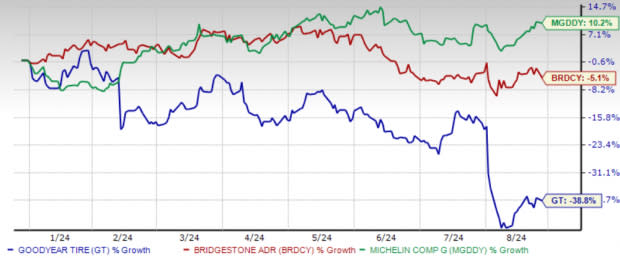

Shares of The Goodyear Tire & Rubber Company GT, one of the largest tire manufacturing companies in the world, have plunged 38.8% year to date to close at $8.76 on Monday. Shares of GT’s competitors Bridgestone Corp BRDCY and Michelin MGDDY are down 5.1% and up 10.2%, respectively.

Goodyear YTD Price Comparison with Competitors

Image Source: Zacks Investment Research

Weaker commercial truck business, high debt level and substantial amounts of investment and capital spending are believed to be the primary factors behind the poor performance of Goodyear stock.

The company’s shares are trading below the 50-day moving average. When a stock trades below its moving average, it could indicate a downtrend or a period of weakness in the stock price.

GT Stock Trades Below 50-Day Average

Image Source: Zacks Investment Research

The company’s shares have seen a major dip year to date. Should you buy it, or is it a risky bet? Let’s find out.

What’s Clouding Goodyear’s Prospects?

High Debt Pile: On June 30, 2024, long-term debt and finance leases rose to $6,832 million from $6,831 million as of Dec. 31, 2023. Notably, Goodyear’s long-term debt-to-capital ratio of 0.58 is higher than the auto sector’s 0.34. Elevated leverage restricts the firm’s financial flexibility.

Soaring Capex to Limit Cash Flows: Technology change requires Goodyear to make substantial amounts of investment and capital spending in order to develop technologically advanced offerings. Capex for 2024 is expected to be around $1.25 billion, up from $1.05 billion in 2023. High spending on account of the upgrades for more complex tire designs and brownfield expansions are likely to clip cash flows.

Inflation: While global inflation is showing signs of gradual decline, it remains above pre-pandemic levels. The company expects non-raw material inflation and other costs to be about $60 million higher in the third quarter of 2024 compared with the year-ago quarter’s period.

Weak Commercial Truck Business: In the commercial truck business, weak fleet industry conditions have impacted the company’s performance. In the first half of 2024, sales totaled $9.11 billion, down 7.1% from last year due to industry weakness. These ongoing challenges are likely to take a hit on the company’s top-line growth in the second half.

GT Witnessing Southbound Estimates

The Zacks Consensus Estimate for GT’s 2024 EPS estimate implies a year-over-year decline of 3.83%. In the last seven days, the company has also seen its EPS estimates decline for 2024 and 2025.

Conclusion

Goodyear’s higher long-term debt-to-capital ratio compared with that of the auto sector, substantial investment and capital spending on technological development and ongoing weakness in the commercial truck business do not make it appealing. Investors are better off avoiding this stock.

Goodyear currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Goodyear Tire & Rubber Company (GT) : Free Stock Analysis Report

Bridgestone Corp. (BRDCY) : Free Stock Analysis Report

Michelin (MGDDY) : Free Stock Analysis Report