As global markets react to the recent Fed rate cut, Hong Kong’s Hang Seng Index has seen a notable uptick, gaining 5.12% in a holiday-shortened week. This positive momentum sets the stage for examining growth companies with high insider ownership, which can be indicative of strong confidence from those closest to the business. In such an environment, stocks with significant insider investment often signal potential resilience and growth prospects, making them compelling options for investors looking to capitalize on current market conditions.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

Laopu Gold (SEHK:6181) |

36.4% |

34.7% |

|

Akeso (SEHK:9926) |

20.5% |

54.7% |

|

Fenbi (SEHK:2469) |

33.1% |

22.4% |

|

Zylox-Tonbridge Medical Technology (SEHK:2190) |

18.8% |

69.8% |

|

Pacific Textiles Holdings (SEHK:1382) |

11.2% |

37.7% |

|

Zhejiang Leapmotor Technology (SEHK:9863) |

15% |

78.9% |

|

DPC Dash (SEHK:1405) |

38.2% |

104.2% |

|

Kindstar Globalgene Technology (SEHK:9960) |

16.5% |

88% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

109.2% |

|

Beijing Airdoc Technology (SEHK:2251) |

29.1% |

93.4% |

Let’s review some notable picks from our screened stocks.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited, with a market cap of HK$802.38 billion, operates in the automobiles and batteries sectors across China, Hong Kong, Macau, Taiwan, and internationally.

Operations: BYD’s revenue segments include CN¥507.52 billion from Automobiles and Related Products and Other Products, and CN¥154.49 billion from Mobile Handset Components, Assembly Service, and Other Products.

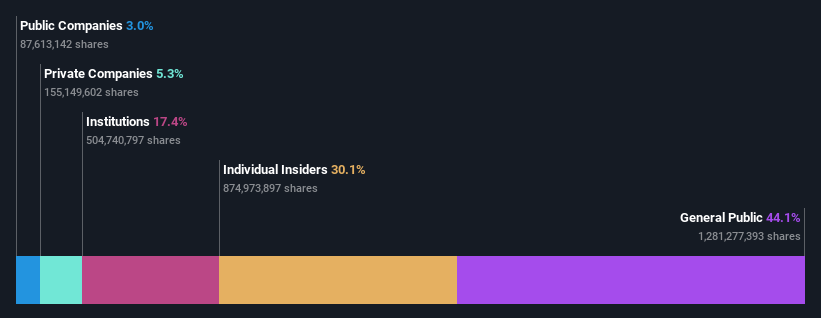

Insider Ownership: 30.1%

Earnings Growth Forecast: 15.2% p.a.

BYD has shown substantial growth with earnings up 36.2% over the past year and revenue forecasted to grow at 14.1% annually, outpacing the Hong Kong market’s average. Recent unaudited production results for August 2024 reported a significant increase in volume year-over-year, reflecting strong operational performance. The company also announced a strategic partnership with Uber to introduce 100,000 new electric vehicles globally, enhancing its market presence and supporting further growth initiatives.

Simply Wall St Growth Rating: ★★★★★☆

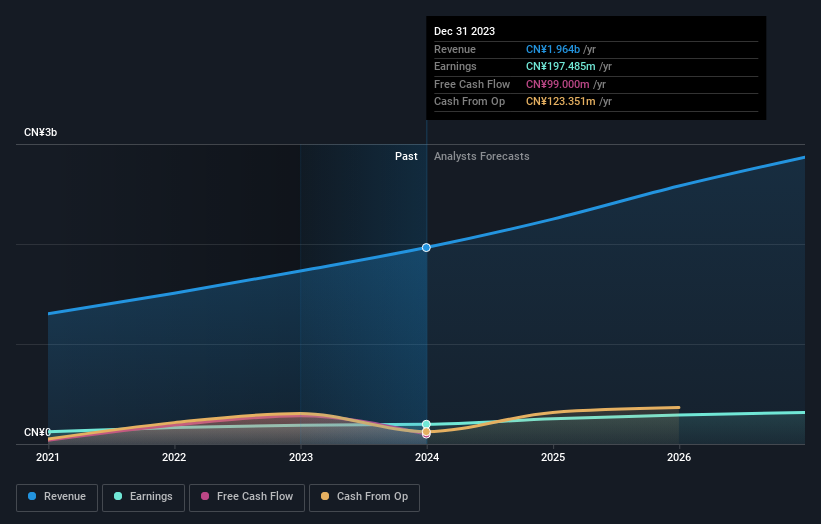

Overview: Xiamen Yan Palace Bird’s Nest Industry Co., Ltd. (SEHK:1497) focuses on the research, development, production, and marketing of edible bird’s nest products in China and has a market cap of HK$6.02 billion.

Operations: The company’s revenue segments include sales to online distributors (CN¥21.07 million), offline distributors (CN¥508.94 million), direct sales to online customers (CN¥907.52 million), offline customers (CN¥344.32 million), and e-commerce platforms (CN¥290.51 million).

Insider Ownership: 26.7%

Earnings Growth Forecast: 23.8% p.a.

Xiamen Yan Palace Bird’s Nest Industry has demonstrated steady revenue growth, reporting CNY 1.06 billion for the first half of 2024, up from CNY 951.2 million a year ago. Despite this, net income fell to CNY 58.08 million from CNY 101.08 million due to increased operational challenges. Insider ownership remains high, indicating confidence in long-term prospects. Analysts forecast a significant annual earnings growth rate of around 23.9%, outpacing the Hong Kong market average.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Meituan operates as a technology retail company in the People’s Republic of China with a market cap of approximately HK$841.32 billion.

Operations: The company’s revenue segments include Core Local Commerce generating CN¥228.13 billion and New Initiatives contributing CN¥77.56 billion.

Insider Ownership: 11.6%

Earnings Growth Forecast: 26% p.a.

Meituan’s earnings grew by 175.5% over the past year, and its revenue is forecast to grow at 12.9% annually, faster than the Hong Kong market average. Despite a lack of substantial insider buying recently, insider ownership remains high. The company has been actively repurchasing shares, completing buybacks totaling HKD 7.17 billion this year alone. Analysts expect Meituan’s earnings to grow significantly at around 26% per year over the next three years.

Turning Ideas Into Actions

Seeking Other Investments?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1211 SEHK:1497 and SEHK:3690.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com