Investors may be surprised to see a comparison between BYD and Tesla.

Electric vehicle (EV) maker BYD (BYDDY) isn’t an automotive start-up. It’s been manufacturing vehicles in China for more than 20 years. Its first new energy vehicle — a plug-in hybrid — was introduced in 2008. BYD then launched a fully battery-powered electric car the next year.

BYD can arguably be called the global EV leader even over Tesla. The Chinese company generates more revenue than Tesla, and it is still growing. One chart may convince investors that its stock is the better buy, too.

Image source: BYD.

BYD’s growth is accelerating

BYD has dominated EV sales in China, but it is now seeing growth in Europe. Registrations for BYD vehicles in Europe soared 225% year over year in July, according to the European Automobile Manufacturers Association. Much of that is at Tesla’s expense, with Tesla registrations down 40% year over year.

BYD is increasing profits, too. In the first half of 2025, net profit grew nearly 14% as revenue climbed 23%. Like Tesla, BYD is facing strong competition globally, and profit margins are under pressure. Unlike Tesla, however, BYD’s new energy vehicle sales hit a record high.

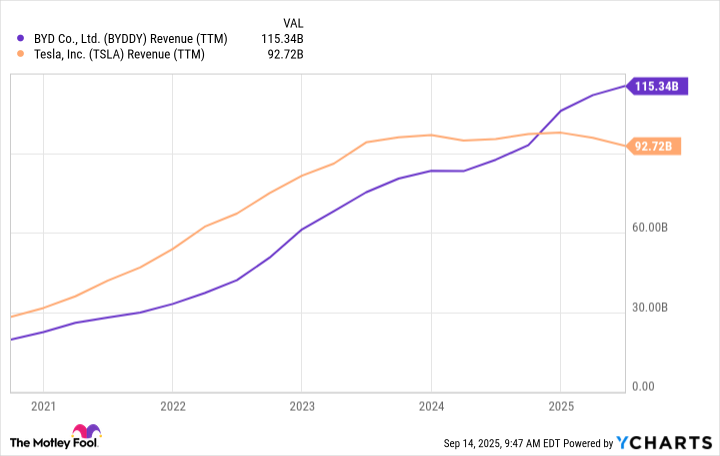

It’s impressive that revenue is growing so strongly from an already high base.

BYDDY Revenue (TTM) data by YCharts

Trailing-12-month (TTM) revenue has surpassed that of Tesla, and the gap is growing. BYD’s revenue growth rate has far outpaced Tesla, too. It soared nearly 500% in the last five years, compared to Tesla’s 230% growth.

It’s impressive to see the growth rate accelerating for a company with over $100 billion in annual revenue. BYD shares have retreated 20% from record highs over the last three months. That drop created a good opportunity to invest in this global EV leader.

Howard Smith has positions in BYD Company and Tesla. The Motley Fool has positions in and recommends Tesla. The Motley Fool recommends BYD Company. The Motley Fool has a disclosure policy.