With the explosion of micromobility in Europe over the past year and InMotion’s focus on the space, I’ve been increasingly asked “Scooters… what’s going on?”.

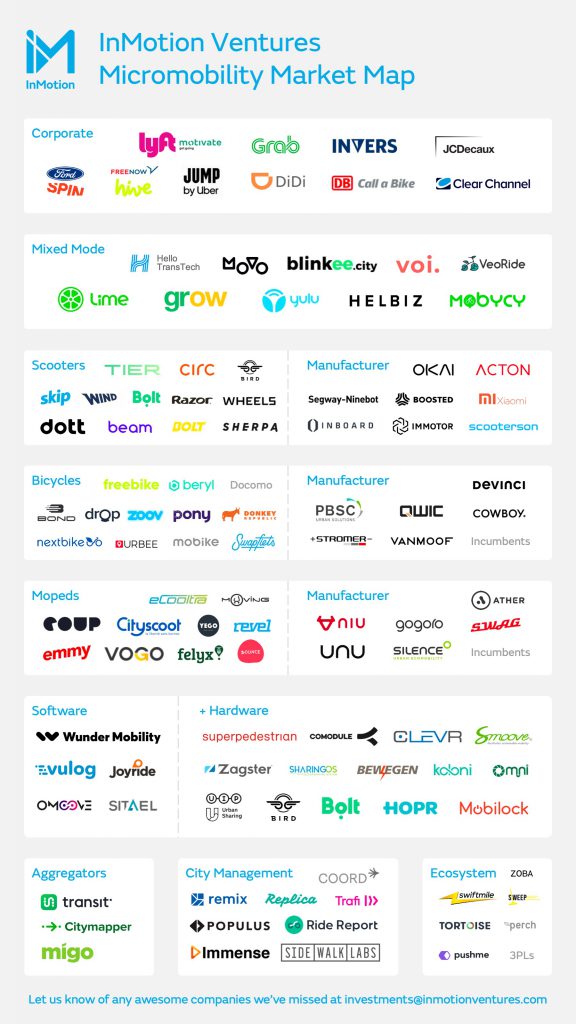

So in an effort to bring some clarity to this rapidly evolving sector, we’ve created a global micromobility market map. We’ve scoured the world for services, software and hardware suppliers and the surrounding ecosystem, as well as checked if the brand names of old are still around (spoiler, many aren’t).

Much has been written about the transformation of city transport, with scooter service adoption rates an order of magnitude greater than ride-hailing in the early days. These services appear to be dominating existing modes for short distance trips and broadening the demographic for shared mobility.

But this transformation is about much more than shared scooters or bicycles. An entire industry is being built around the shift to light electric vehicles and their role in the future of cities.

In mapping the market, we’ve seen corporates building and acquiring, existing players going multi-modal, a hardware industry for shared vehicles booming, and software companies offering out of the box solutions. We’re seeing aggregators consolidating the ten apps on our phones, city management solutions making sense of the melee for transit agencies, and a supporting ecosystem emerge around the industry, from charging stations to autonomous scooter technology.

A few interesting nuggets from our research:

- A year on from their acquisition of Jump, Uber said they are seeing the bike-sharing service cannibalise their short distance ride-hailing business, with their micromobility customers hiring 10% fewer cars through the app. However, they clearly see this as a route to owning their customers’ mobility spend, with a $1 billion budget in 2019 for scooters, bikes and other mobility initiatives.

- On hardware: In the beginning, scooter lifetimes were in the region of 1-2 months, creating depreciation costs per scooter per day that would never give positive contribution margins. Since then, these companies have invested heavily in hardware, learning from their experience to-date to design robust and bespoke scooters with the likes of Okai. The next iteration of these scooters will likely include swappable batteries in order to reduce logistics costs and keep scooters out on the streets longer.

- On software: Whilst the bigger players will always look to keep their product in house, software and turnkey providers are making it easier for startups, corporates, municipalities and campuses to operate their own fleets. With Wunder Mobility recently raising another $30 million for their multi-modal asset sharing platform, and Bolt and Bird offering a franchise-style turnkey solution, the barriers to rolling out a local service are lower than ever before.

- Aggregation is becoming more and more relevant. Since InMotion invested in the journey planning and aggregation app Transit last year, the number of micromobility companies globally has grown by an order of magnitude.

At the time, Transit were offering a multi-modal planning experience with payment options on ride-hailing. Since then, they’ve added many micromobility options and deepened their relationship with public transport operators to offer a holistic planning and payment experience across many modes.

However, recently some of the mobility services have shut down their APIs to stop aggregation. We think this is likely part of a move to create their own ecosystems where they can drive retention through subscription and loyalty programmes.

That said, we believe that in the future, cities will be mandating open standards in the interest of consumer choice, with aggregators well positioned to give consumers the best transportation experience.

- On cities: With numerous services deploying and cities beginning to regulate more heavily with permit and license systems, they need tools to manage their streets. Notably, Google’s Sidewalk Labs has now successfully spun out two companies in Coord and Replica, who are helping cities to plan and manage their kerbside assets more effectively. Remix, Populus and a host of early-stage businesses are also releasing products to help cities work with micromobility services.

Looking to the future, we’re optimistic about micromobility’s potential to play a key role in how we transport ourselves around cities, offering an environmentally friendly, congestion-reducing and affordable transportation option for all.