A 3D printed Zoom logo is placed on the keyboard in this illustration taken April 12, 2020. REUTERS/Dado Ruvic/Illustration/Files

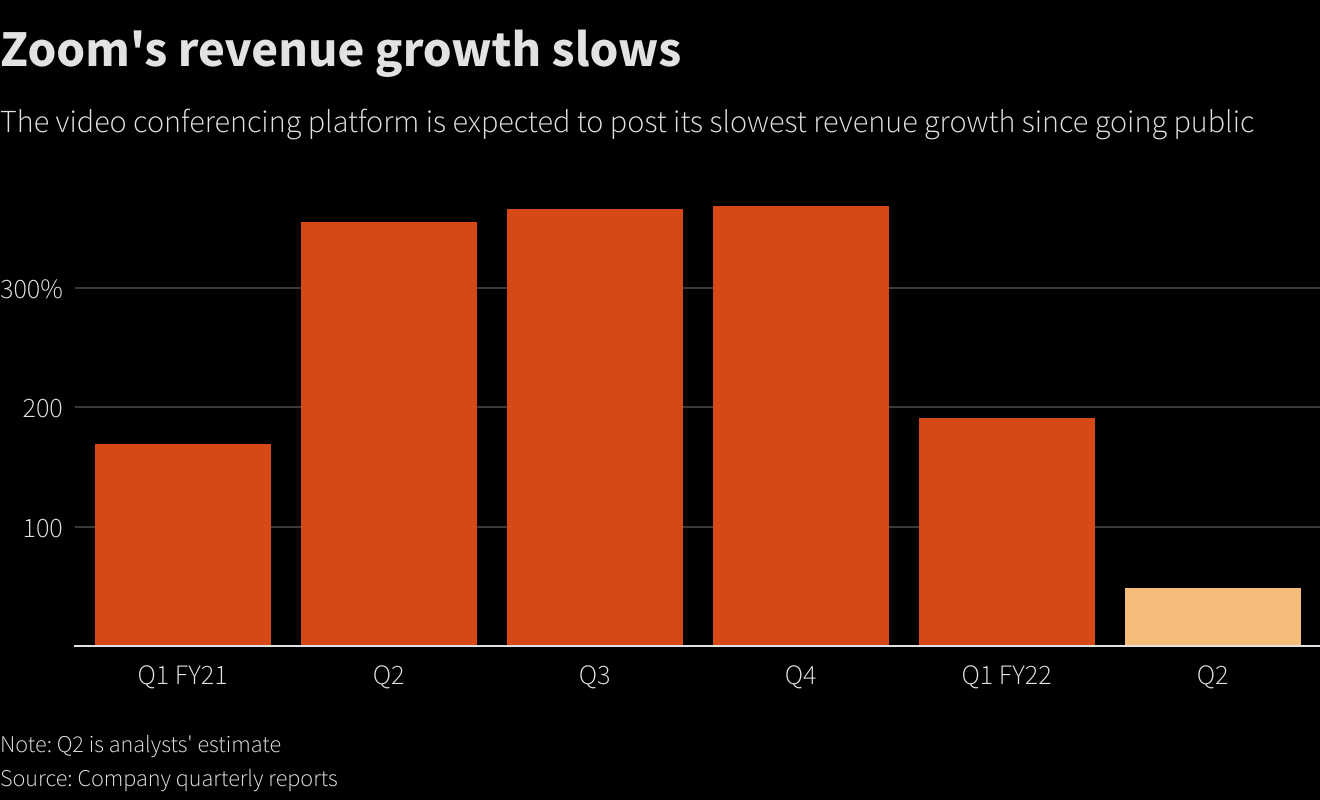

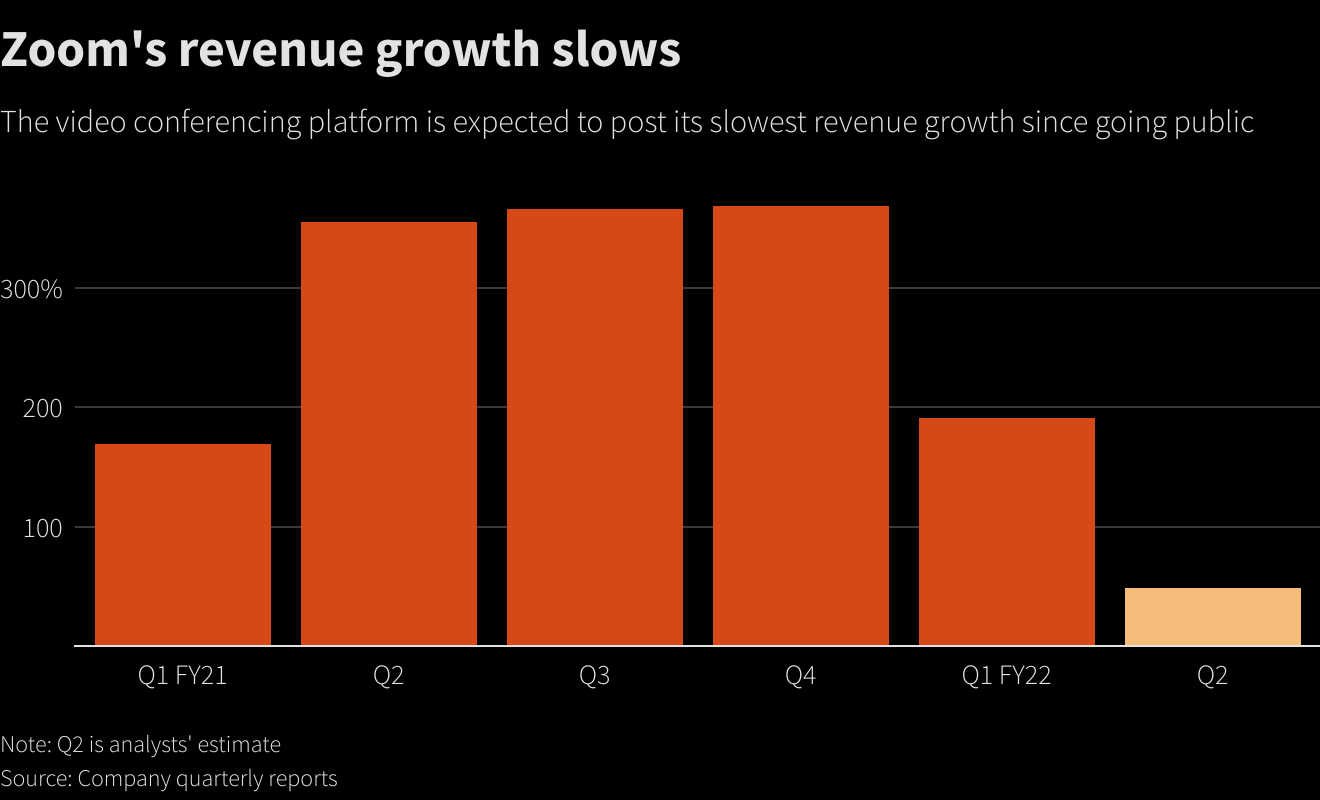

Aug 30 (Reuters) – When stay-at-home favorite Zoom (ZM.O) reports quarterly results on Monday, Wall Street will look for details on how the video conferencing platform plans to attract more users as its meteoric growth brakes to its slowest rate since going public.

Zoom’s revenue growth has been decelerating as the economy slowly reopens, users complain of “Zoom-fatigue” and as vaccinated people return to school and offices.

Wall Street analysts expect revenue to grow only 49% in the to-be-reported quarter, compared with multiple-fold growth rates in the past year.

Zoom raked in millions of new users as the pandemic forced more people to work, study and communicate with friends and family remotely.

The company is now looking to win bigger contracts from businesses, an area dominated by rivals like Cisco (CSCO.O), Microsoft’s (MSFT.O) Teams and Salesforce’s (CRM.N) Slack.

“Long term, we expect Zoom will grow into a broader enterprise communication and collaboration platform,” said Rishi Jaluria, RBC Capital Markets analyst.

THE CONTEXT

“The company’s ‘Act 2.0’ is Zoom Phone,” Piper Sandler analyst James Fish said. “We’re seeing a massive acceleration in on-premise to cloud-based voice solutions, which favors vendors like Zoom.”

Zoom Phone is a cloud-based phone system, which allows users to make calls across devices and help businesses manage activities like queuing and recording calls in-house. It has more than 400,000 customers.

Over the last two months, Zoom has said it would buy Kites GmbH, a firm that helps in real-time language translation and announced its largest deal – a $14.7 billion buyout of cloud-based call-center software provider Five9 to double down on the service. read more

“The enterprise side of the market is only 15% migrated to cloud phones,” says Needham analyst Ryan Koontz.

However, Zoom faces a two-pronged challenge with fierce competition from Cisco, Microsoft and Salesforce and the post-pandemic weakening in user traffic growth, although a hybrid working world is likely to keep demand up.

THE FUNDAMENTALS

* Analysts estimate Zoom’s second-quarter revenue to grow 49% to $991 million.

* Earnings per share is estimated at $1.16

* Its shares have gained ~1% year-to-date, while the benchmark S&P 500 index (.SPX) has gained about 20%

* The stock surged over 395% in 2020

WALL STREET SENTIMENT

* Wall Street analysts are largely bullish, with 15 out of 28 rating the stock “buy” or higher, while 12 have a “hold” rating and one rates it as a “sell” or lower.

* The median price target is $429.50 versus the current price of $340.81

Reporting by Chavi Mehta and Eva Mathews in Bengaluru; Writing by Subrat Patnaik; Editing by Arun Koyyur

Our Standards: The Thomson Reuters Trust Principles.