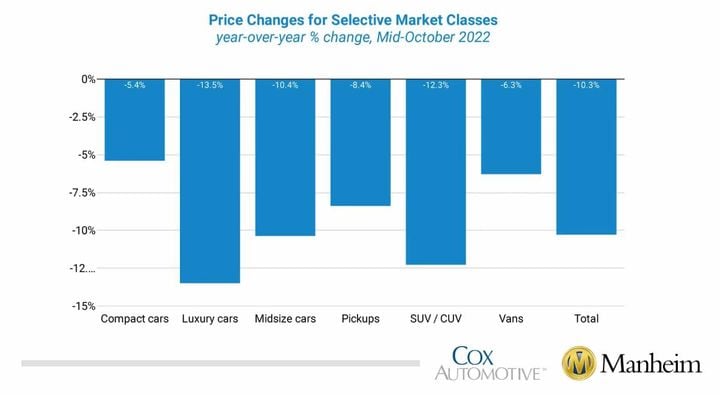

Compact cars had the lowest decline at -5.4%, while vans and pickups lost less than the overall industry in seasonally adjusted year-over-year changes.

Graphic: Cox Automotive / Manheim

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) declined 2% from September in the first 15 days of October, according to the Manheim Used Vehicle Value Index, which fell to 200.5 and was down 10.3% from October 2021.

The non-adjusted price change in the first half of October was a decline of 1.8% compared to September, moving the unadjusted average price down 9% year over year.

During the last two weeks, Manheim Market Report (MMR) prices saw lower-than-normal and slowing declines resulting in a 1.1% cumulative decline in the Three-Year-Old MMR Index, which represents the largest model-year cohort at auction. Over the first 15 days of October, MMR Retention, which is the average difference in price relative to current MMR, averaged 98.2%, which indicates that valuation models are ahead of market prices. The average daily sales conversion rate of 60% in the first half of October increased relative to September’s daily average of 48.8%, and conversion rates typically decline in October. The latest trends in key indicators suggest wholesale used-vehicle values should decline less than normal in the second half of October.

All eight major market segments saw seasonally adjusted prices that were lower year over year in the first half of October. Compact cars had the lowest decline at -5.4%, while vans and pickups lost less than the overall industry in seasonally adjusted year-over-year changes. Six major segments saw price decreases compared to September, with full-size cars and vans showing gains of 10.2% and 0.2%, respectively. All major segments also saw unadjusted price declines in the first 15 days of October.

Retail and Wholesale Days’ Supply Tighter Than Normal in Mid-October

Using estimates based on vAuto data as of Oct. 10, used retail days’ supply was 49 days, which was down one day from the end of September. Days’ supply was up nine days year over year but down one day against the same week in 2019. Leveraging Manheim sales and inventory data, we estimate that wholesale supply ended September at 28 days, unchanged from the end of August but up nine days year over year. As of Oct. 15, wholesale supply was at 28 days, unchanged from the end of September but up 10 days year over year and four days lower than at the same time in 2019. Used supply measured in days’ supply and compared to 2019 suggests supply is tighter than normal for this time of year, which indicates that depreciation should be lower than normal for the time of year as well.

Rental Risk Prices Decreasing Along with Overall Wholesale Market

The average price for rental risk units sold at auction in the first 15 days of October was down 4.5% year over year. Rental risk prices were down 3.4% compared to the full month of September. Average mileage for rental risk units in the first half of October (at 57,000 miles) was down 6% compared to a year ago but up 5.3% month over month.

Consumer Sentiment Appears Stronger to Start October

The initial October reading on Consumer Sentiment from the University of Michigan increased by 2% to 59.8 from improving views of current conditions. Future expectations declined. Expected inflation rates increased in the October survey, which is a concern for the Fed and their campaign to reduce inflation. Consumers’ views of buying conditions for vehicles improved and were tied with March for the second-best reading this year. June was the all-time low in the reading. The daily index of consumer sentiment from Morning Consult reflects that sentiment may not be so strong. The timelier measure indicated consumer sentiment was down 1.4% in the first 15 days of October. This lower measure coincided with increasing average gas prices in early October and a turbulent stock market delivering new lows for the year on major indices.

Originally posted on Vehicle Remarketing