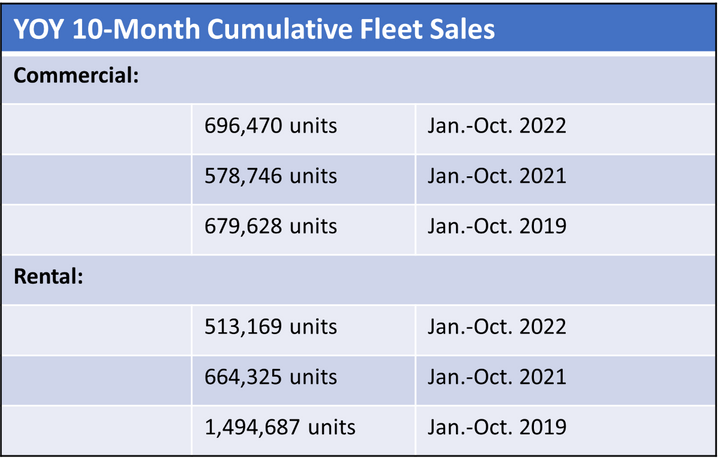

For commercial fleets, cumulative sales for 2022 represented a 20.3% increase over 2021 — and 2.5% over 2019. On the rental side for the same period, sales are still underwater to 2021 and an even greater percentage — 66% — lower than 2019.

Data: Bobit

We have 10 months of U.S. fleet sales under belts, which represents a good indicator of how the market is progressing this year in the return to normal — or, more precisely, the quest for a new normal.

The data shows positive trendlines but diverge depending on fleet types. So before digging into the fleet sales numbers that Bobit collects, it’s relevant to outline the differences between sales to commercial, rental, and government fleets.

Sales Differences Between Fleet Types

- Car rental companies fleet more than twice the number of commercial units in a given normalized year. For instance, in 2019 1.74 million vehicles were sold into rental, while 800k were sold to commercial fleets. (Government fleet sales are much lower than that on a yearly basis — totaling 254k for 2019.)

- Commercial fleet sales are fairly consistent month to month, with about 60,000 to 80,000 units sold in any given month in a normal year and a mild swell in Spring.

- Rental fleet sales on the other hand are more seasonal, with much bigger sales spikes in the Spring to meet summer demand. Fleet sales to rental range from a high of about 200,000 units in March to a low of about 85,000 units in July.

- Rental fleet sales consist mostly of passenger cars and some trucks, while commercial fleet sales are predominantly trucks with a much smaller percentage of cars.

- Rental fleets keep their vehicles for six to 18 months generally, while commercial fleets run vehicles from 36 months to five and seven years – and longer.

As the largest fleet acquisition entity outside of the federal government, rental fleets had been traditionally able to buy vehicles at as close to “triple net” of invoice – what a dealer pays for vehicles – as any type of buyer.

In the last few years automakers have been public on their intent to limit rental fleet sales while supplying commercial and government fleets as best they can. There has been a traditional perspective that rental fleets can damage a model’s residual value with their shorter cycles and opportunity to flood the secondary market with cars.

The reality is a bit more complicated, though any fleet consignor with the ability to put thousands of cars into the secondary market at a given time can move pricing. This traditional assumption has been turned on its head in this new supply-constrained environment, as even rental companies had to, for a time, pay over MSRP for vehicles.

2022 Year-Over-Year Fleet Sales

Now to the year-to-date sales numbers.

In a tangible sign that the supply crunch is easing, sales to commercial fleets were up over 2021 in every month to date. A 3.8% increase in January 2022 increased to a cumulative 11.6% gain by July and an overall increase of 20.3% through October.

A better indicator of a positive market correction is comparing sales to the same period in 2019, our last benchmark “normal” year. Comparing commercial fleet sales to date in 2022 compared to the same period in 2019 reveal a 2.5% increase over the same period.

On the rental side, sales are trending in the right direction as well, but are still underwater to both 2021 and 2019.

Month over month, rental fleet sales started 2022 in January at a 61.3% deficit to January 2021. That percentage steadily improved month to month. By October, the cumulative gap was down to “only” 22.8% compared to 2021. However, rental sales over the first 10 months of this year are still at a whopping 66% deficit to the same period in 2019.

Regarding government fleet sales, year-to-date sales of 162,219 are 5.8% over the same period in 2021, yet that’s 24.5% fewer units sold than in 2019.

Overall, the numbers show positive trends, but a stark contrast by fleet type. While commercial fleet sales have returned to normal patterns, rental fleet sales have not. It remains to be seen if this present pattern will turn into a “new normal” for rental fleets.

Positive Signs in October SAAR

The uptick in fleet sales mirrors an increase in the overall market.

The U.S. seasonal adjusted annual rate (SAAR) for October is 15.1 million units, up from 13.4 million in September, according to data from LMC Automotive. That’s only the second time that the rate has exceeded 15 million units per year in 2022.

“While the industry continues to face challenges on a number of different fronts, some encouragement can perhaps be drawn from the October results,” said David Oakley, manager, Americas sales forecasts for LMC Automotive, a press statement.

“The 15 million units-per-year mark has only been surpassed twice since the first half of 2021, providing some cheer heading into the final two months of 2022,” he continued. “Inventory levels have improved notably over the last two months, relieving some of the pressure on the supply side of the market.”

Oakley cautioned that progress may not be linear, as logistical problems, rising interest rates and financing costs, and average transaction prices still at near-record levels could negatively affect the market.

Originally posted on Automotive Fleet