While India isn’t at risk of a recession due to rising borrowing costs, excessive monetary tightening can expose the economy to below-potential growth that can cripple job creation and productivity, warns a rate-setter.

“What I am worried about is sub-par growth after two lost years,” Jayanth R Varma, a member of the Reserve Bank of India’s rate panel, said in an email interview, referring to the time lost to the pandemic.

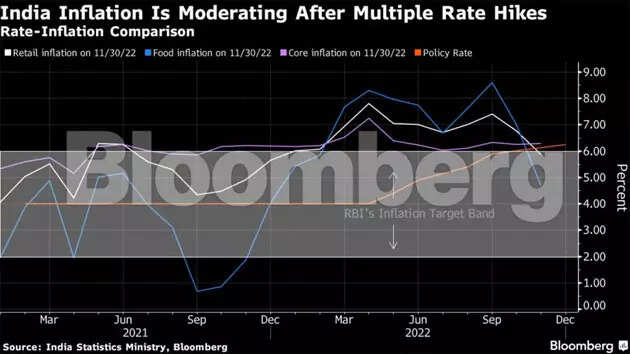

Known for his hawkish comments in the past, Varma opposed both the size of the RBI’s latest interest-rate increase, as well as its continued tightening bias. The central bank increased the key rate by 35 basis points to 6.25% at its meeting earlier this month, taking the total hikes to 225 basis points this year.

“India is at a demographic stage where the workforce is growing rapidly, and we need a certain level of growth to create new jobs for the fresh entrants into the labour market,” he said. “My worry is that excessive monetary tightening might cause us to fall short of this aspirational goal.” India’s $3.18 trillion economy expanded 6.3% from a year ago in the quarter to September, down from 13.5% in the previous three months. The deceleration comes amid fears of slowing global economic growth due to restrictive monetary policy to curb inflation.

India’s $3.18 trillion economy expanded 6.3% from a year ago in the quarter to September, down from 13.5% in the previous three months. The deceleration comes amid fears of slowing global economic growth due to restrictive monetary policy to curb inflation.

Many analysts see India, which is poised to soon overtake China as the world’s most populous nation, as having the potential to grow at a sustained 7% pace, with Bloomberg Economics seeing that rate ascending to 7.6% by 2026 and peaking around 8.5% in the early 2030s.

That pace of expansion is not a choice, but a necessity for India in order to generate jobs for the more than 10 million young people entering the workforce each year and reduce poverty. It’s also key to boosting its per capita income, which according to London-based data analysis company CEIC Data, is currently below Bangladesh’s $2,723.

In the minutes of the latest policy meeting, Varma described the current 6.25% level of the repurchase rate as posing “an unwarranted risk to economic growth.” He had earlier estimated 6% to be sufficient to contain inflationary pressures.

His comments come at a time when unemployment is seen rising in India despite a good monsoon supporting farm activity. India’s joblessness in December climbed to over 8%, the highest since the nationwide lockdown in March 2020, according to data from Centre for Monitoring Indian Economy Pvt. Ltd.

Varma, in the interview, said rate hikes done in the latter part of the year will start having an effect in another quarter or two. “I am confident that in ensuing months, as this aggressive tightening depresses demand, inflation will come down significantly and move closer to the target.”

Here are other key comments from Varma:

- India’s macroeconomic situation calls for a different balance between growth and inflation at this point where a large amount of front-loaded tightening has already been completed

- Says he believes that the MPC has a robust decision making process, and is perfectly capable of making mid-course corrections in response to the emerging evidence. “Therefore, I do not see any threat to the credibility or independence of the MPC”

- Says last few months have seen a sharp reversal of risks to inflation and growth