[1/4]A worker looks on at the Niska trial graphite mine, owned by Talga Group, which aims to launch commercial production in 2024, in Norrbotten, northern Sweden, in this handout image taken in August 2022 and obtained by Reuters on June 15, 2023. Tomas Bergman/Handout via REUTERS

LONDON, June 21 (Reuters) – Automakers, including Tesla and Mercedes, are rushing to lock in graphite supply from outside dominant producer China, as demand for electric vehicle (EV) batteries outpaces other uses for the mineral for the first time due to soaring EV sales.

Auto firms have been slow to plan for graphite shortages, focusing mainly on better-known battery materials lithium and cobalt, even though graphite is the largest battery component by weight.

Now, car makers are knocking at the doors of new producers, such as Madagascar and Mozambique, as this year EVs are forecast to account for more than 50% of the natural graphite market for the first time, according to consultancy Project Blue.

Shortages of material produced outside of China will be even more acute as legislation in the United States and Europe aims to cut reliance on China for critical minerals.

“Automakers are in a real bind because there’s been no investment in Western graphite,” said Mark Thompson, founder and managing director of Australia’s Talga Group Ltd (TLG.AX), which plans to launch production next year in Sweden.

Each EV on average needs 50-100 kg of graphite in its battery pack for the anodes, the negative electrodes of a battery, about twice the amount of lithium.

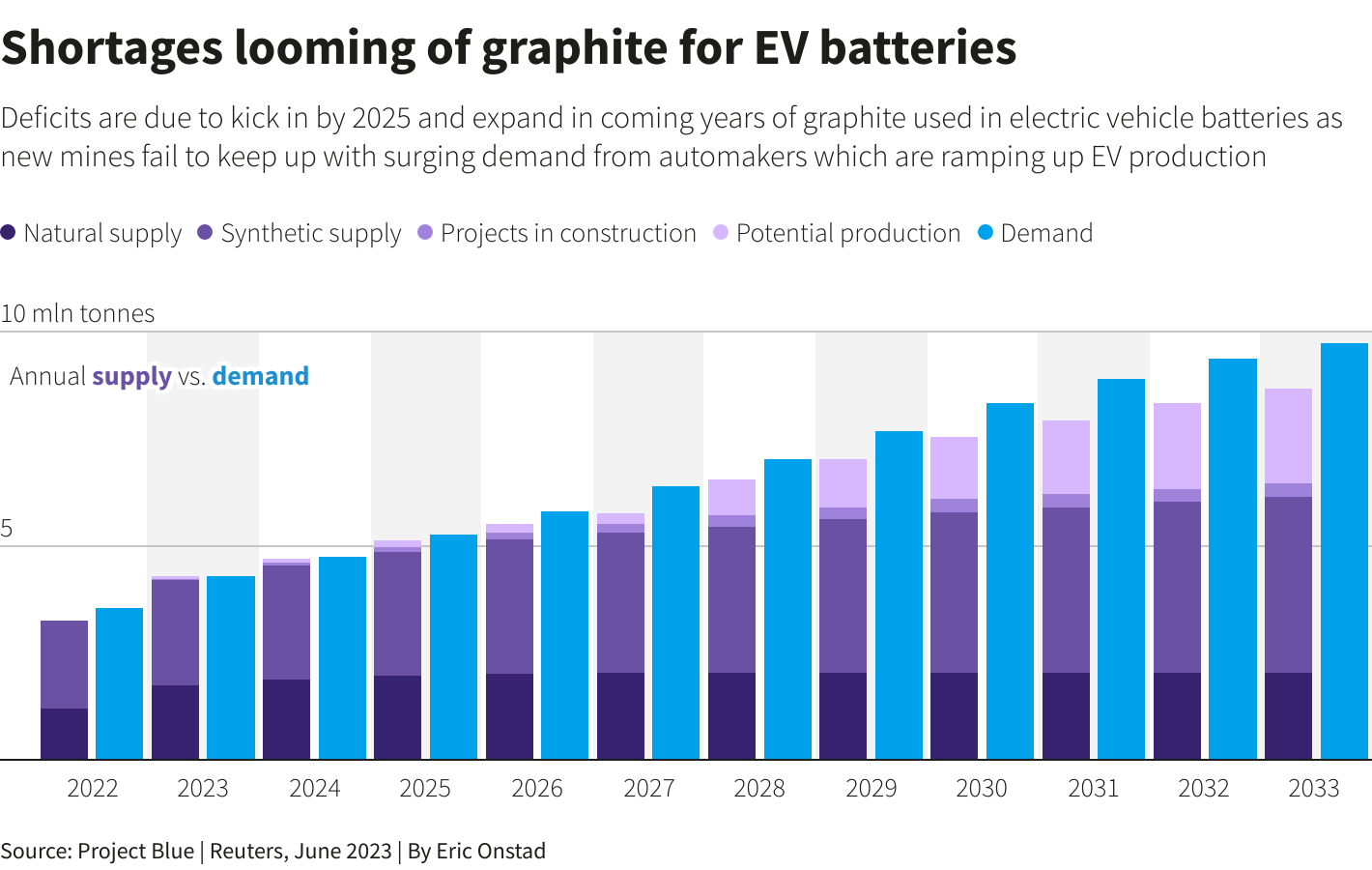

The main use of graphite has been in the steel industry, but EV sales are due to more than triple by 2030 to 35 million from 2022, BMO Capital Markets forecasts.

Graphite shortages are expected to rise in coming years, with a global supply deficit of 777,000 tonnes expected by 2030, Project Blue projections showed.

About $12 billion of investment is needed by 2030 in graphite and 97 new mines required by 2035 to meet demand, Benchmark Mineral Intelligence (BMI) said in a report.

China produces 61% of global natural graphite and 98% of the final processed material to make battery anodes, BMI said.

SUPPLY DEALS

Talga group is seeking to supply automakers, such as Tesla, Toyota and Ford, as well as battery producers such as Sweden’s Northvolt, Thompson told Reuters.

Tesla Inc (TSLA.O) and Northvolt did not reply to a request for comment while Toyota Motor Corp (7203.T) and Ford Motor Co (F.N) declined to comment.

Talga has already signed non-binding supply agreements with two European battery makers that have links with Mercedes-Benz (MBGn.DE), Stellantis (STLAM.MI) and Renault (RENA.PA).

Mercedes said it was diversifying the sourcing of raw materials, including graphite, and “have been in dialogue with various suppliers for some time”.

“All the car companies are now scrambling to understand how to source battery materials at the mine level,” said Brent Nykoliation, executive vice president of NextSource Materials.

NextSource (NEXT.TO), which in April commissioned a mine in Madagascar, is also in talks with auto companies, but said the details were confidential.

Tesla has been at the forefront in securing graphite, having already agreed deals with Syrah Resources (SYR.AX), which operates a mine in Mozambique, and with Magnis Energy Technologies (MNS.AX).

Syrah is building a U.S. processing operation, one of a handful of plants being built outside of China that can transform graphite for battery use.

NextSource is building a processing plant in Mauritius while Talga plans to construct a factory in Sweden.

CHINA DOMINATES

Western processing operations, however, will grow slowly.

“China is still incredibly dominant in the graphite space and we anticipate they will maintain dominance for years to come,” said George Miller, senior analyst at BMI.

By 2032, China will still control 79% of production of a type of processed graphite – uncoated spheroidised purified graphite – compared to 100% in 2022, according to BMI.

This Chinese influence on the market may make it difficult for automakers who want to qualify for EV subsidies under the U.S. Inflation Reduction Act.

The IRA requires certain high percentages of battery components to be produced in the United States, or in a country with which it has a free trade deal.

The European Union has proposed legislation that aims to reduce dependency on any one country for any key raw material to 65% by 2030.

Agreeing graphite supply deals is complex, requiring extensive safety testing for material going into each model of EV that can take up to three years.

CARBON FOOTPRINT

Western auto groups are focusing on deals with graphite mines partly because it is around 55% less carbon intensive to produce anodes with natural material compared to synthetic graphite made from petroleum products.

Natural graphite anodes tend to be cheaper and are beneficial for cell capacity and power output, allowing cars to run further distances before charging.

There is also expected to be competition with the steel industry, said analyst Reitumetse Chalale at Project Blue.

Another anode ingredient is silicon, which also enables an EV to drive longer distances before recharging.

Currently, the maximum amount of silicon added to batteries is about 10% because the material expands during use and can degrade the battery.

Companies are working on technology that would allow larger amounts of silicon. If successful, that could be a threat to graphite in the long term.

Reporting by Eric Onstad; Editing by Veronica Brown and Sharon Singleton

Our Standards: The Thomson Reuters Trust Principles.