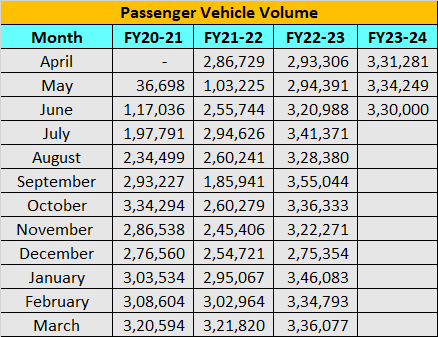

It is going to be a bittersweet June for the Indian passenger car market. Despite registering the highest number of June dispatches ever at 3.25 to 3.30 lakh units, Autocar Professional learns that the growth rate for the month is expected to fall to 2.5-4 percent, which is the lowest growth rate in fifteen months. At one point, the highest growth rate was 90.94 in September 2022.

The high base effect of June 2022 and the parts shortage for fast-selling models have pulled down the growth to a low single digit, thereby offering a reality check for the passenger vehicle industry. The growth rate for the April to June quarter too is expected to come down to eight percent closing at a shade near one million units, say industry sources. For 12 of the past 15 months, automakers have dispatched over three lakh units per month, indicating that the base has become high.

Shashank Srivastava, Senior Executive Officer, Sales and Marketing at Maruti Suzuki told Autocar Professional, “The demand and booking is holding well and the traction in the market is better than expected, however, the base is catching up and that should reflect on the growth rate this month as well the quarter.”

Supply constraints owing to the shortage of semiconductor components availability and the week-long maintenance shut down at the plant obviously led to lower vehicle availability for wholesales. Pending bookings for the market leader is expectedly at 3.92 lakh.

Along with Maruti Suzuki, the likes of Mahindra & Mahindra (M&M), Toyota Kirloskar too continues to have record booking levels and the shortage of parts continues to lead to a very long waiting period of certain models.

M&M was sitting on pending bookings of over 2.92 lakh units and Toyota Kirloskar continues to have a strong traction for its Hyryder and Hyrcross, with cumulative bookings crossing over one lakh units.

Srivastava says, due to a skew in the semiconductor components availability, there is a clear mismatch in the demand and supply equation across different models. While some models are seeing long waiting periods, there are other models where the inventory increases have led to higher discount levels.

The correction in growth rate happens at a time when the industry inventory is swelling to almost pre-pandemic levels of 40-45 days, claim dealers.

While the demand parameters of inquiries and bookings remain stable there are some fears of it softening due to the higher interest rates and the increasing fear that El Niño may result in a disturbed and skewed monsoon pattern.

The SUV sales continue to drive monthly volumes, however there is a significantly higher stock of hatchbacks and sedans which are comparatively moving slow off the mark. Not surprisingly the discounts for the month of June have increased and there are deals and discounts emerging on the SUVs too. The industry stock is set to reach 2.75 lakh units which is probably the highest inventory witnessed in almost three years.

With inventories rising, hardening interest rates, and fears of El Nino coming true, the market is entering a critical July to September – which is invariably a soft quarter, before momentum picks up in the festive season.

The industry body Society of Indian Automobile Manufacturers Association has already guided for a growth of five to seven percent for passenger vehicles in FY24 and the Q1 growth has already slipped to eight percent despite Q1 turning out to be the best ever Quarter One.

Manish Raj Singhania, President of the Federation of Automotive Dealers Association says, “It’s time automakers see the reality and improve their product assortment and model mix that they are dispatching to dealerships to focus on fast-moving models rather than saddling dealers with low selling inventory.”

The FADA President assures that the demand is still holding strong and the market will grow — but pent-up demand has been exhausted long back — leading to a high cancellation rate, with supplies improving.