June was another positive month for new car registrations in Europe, rounding off what has been a healthy first half of the year in terms of volume. According to JATO Dynamics data across 28 European markets, H1 2023 saw the most registrations since the Covid-19 pandemic with 6.56 million units. This is an increase of 976,000 units compared to H1 2022, and 80,000 units from the same period in 2021. However, the results for 2023 so far were not as high as those in H1 2019 and 2018, with 1.86 million and 2.13 million more units registered respectively in those years.

Felipe Munoz, global analyst at JATO Dynamics, commented: “Although registrations are slowly rising again, difficulties with supply chain, as well as other post-pandemic factors, means that the market won’t return to the same state that it was in before 2020 for a while.” A major barrier to reaching those higher volumes is the accessibility of electric vehicles and their higher prices.

Tesla dominates BEV sales, Model Y best-selling model

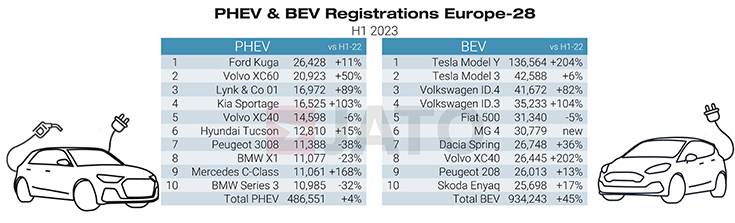

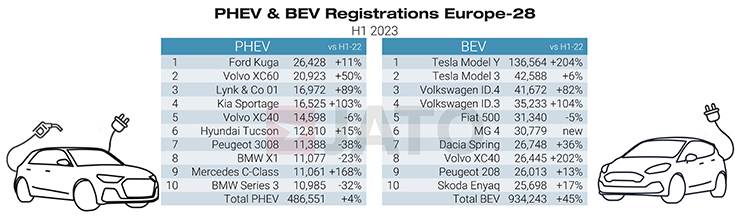

Tesla was the best-seller within the BEV market in both June and H1 of the year more generally, with 48,200 vehicles registered last month – doubling the volume recorded during the same period a year previous. The Tesla Model Y drove the continued popularity of the brand, becoming Europe’s best-selling passenger car in June and H1 2023, as well as reigning as the world’s most popular car in Q1 of the year.

Last month, Tesla registered more new cars than other mainstream brands like Opel/Vauxhall, Citroën, or Fiat, with volume of the Model Y and Model 3 growing by 95% and 117% respectively. Tesla’s performance in June enabled the OEM to achieve the biggest market share increase. Tesla’s market share soared by 1.3 percentage points between H1 2022 and H1 2023, rising from 1.53% to 2.82% – the biggest increase among the 116 brands tracked by JATO in Europe.

Tesla’s success has grown rapidly over the last few years, considering that its market share in H1 2019 amountedto just 0.54%. Munoz noted: “The increase in availability of cars following the start of local production in Germany, as well as price cuts, explains Tesla’s rapid growth recently. It’s also important to note that Tesla represents EVs for many all over the world, and today more and more people are turning electric.”

MG registers second highest market share

Recently, MG has also been shaking the European car market. Once a British brand, all of its current cars are designed, developed, and produced by SAIC, one of China’s biggest OEMs. With 104,300 units registered in H1 2023, MG outsold other major brands such as Mini, Cupra, and Jeep. Partly due to the success of the MG 4, its volume grew by 128% since H1 2022, providing MG with the second highest market share increase in the first half of this year. Munoz added: “MG is using both the notoriety of the brand in the West, and the competitiveness of the Chinese market, to its advantage. Its appealing, modern, and affordable electric cars in both Western and Eastern markets is a good showcase of how Chinese manufacturers can gain more traction and shift perceptions of their products.

Chinese OEMs struggle to outpace competitors

Aside from MG, China’s carmakers are gaining traction less quickly than analysts anticipated. According to Munoz: “The dominating narrative at the moment is around the big potential of Chinese manufacturers in Europe. The potential is certainly there, but the volume of registrations are not currently reflecting that.” JATO’s data shows that of the 26 Chinese-made cars that sell in Europe, 43,101 units have been registered between January and June 2023, amounting to just a 0.66% market share. Nonetheless, they still experienced growth – they had just 0.43% market share during the same period the year before. Including MG, the market share of Chinese OEMs is 2.25%, or 147,394 units.

Munoz added: “It is not easy to continuously grow in such a competitive market, particularly when the brand is unknown and the product needs time to become popular with consumers. The perception of cars by Chinese manufacturers in the West needs to shift in order to see growth.”

Tesla Model Y, with 136,564 units, was the best-selling car in Europe in first-half 2023, ahead of the Dacia Sandero and Volkswagen T-Roc.

Tesla Model Y, with 136,564 units, was the best-selling car in Europe in first-half 2023, ahead of the Dacia Sandero and Volkswagen T-Roc.

Best-sellers: Tesla’s Model Y leads again

Since September 2022, the Tesla Model Y has climbed the monthly European model ranking, topping the list in November, December, February, March, and June. Also what’s worth noting is that the gap between the first and second positions in the overall rankings for both Q1 and H1 2023 has widened from 11,481 units to 13,156 units. The Model Y ranked first in Denmark, Netherlands, Norway, Sweden and Switzerland. It was most popular in Norway, where almost 1 in 4 of new cars registered were Tesla Model Ys.

The Dacia Sandero remained second on the European ranking, with registrations up by 27% to 123,400 units. Interestingly, it is virtually the antithesis of the Model Y – a combustion powered, small, cheaper hatchback. Its place as second in the overall ranking indicates the income differences across regions. In France, for example, the Tesla Model Y was almost 37,000 euros (or 231%) more expensive than the Dacia Sandero.

The Skoda Octavia also experienced a big market share increase from H1 2022 to the same period in 2023. This was followed by the Dacia Jogger, Toyota Yaris Cross, Renault Clio, Volkswagen Tiguan, Renault Megane, MG ZS, Volkswagen ID.3 and ID.4, and Ford Focus. In contrast the models that saw the largest declines were the Toyota RAV4, Peugeot 208, Toyota Corolla, Opel/Vauxhall Crossland, Fiat Panda, Citroën C3, Peugeot 3008, Volksagen Golf, Renault Zoe, and Kia Niro.

All data charts: JATO Dynamics