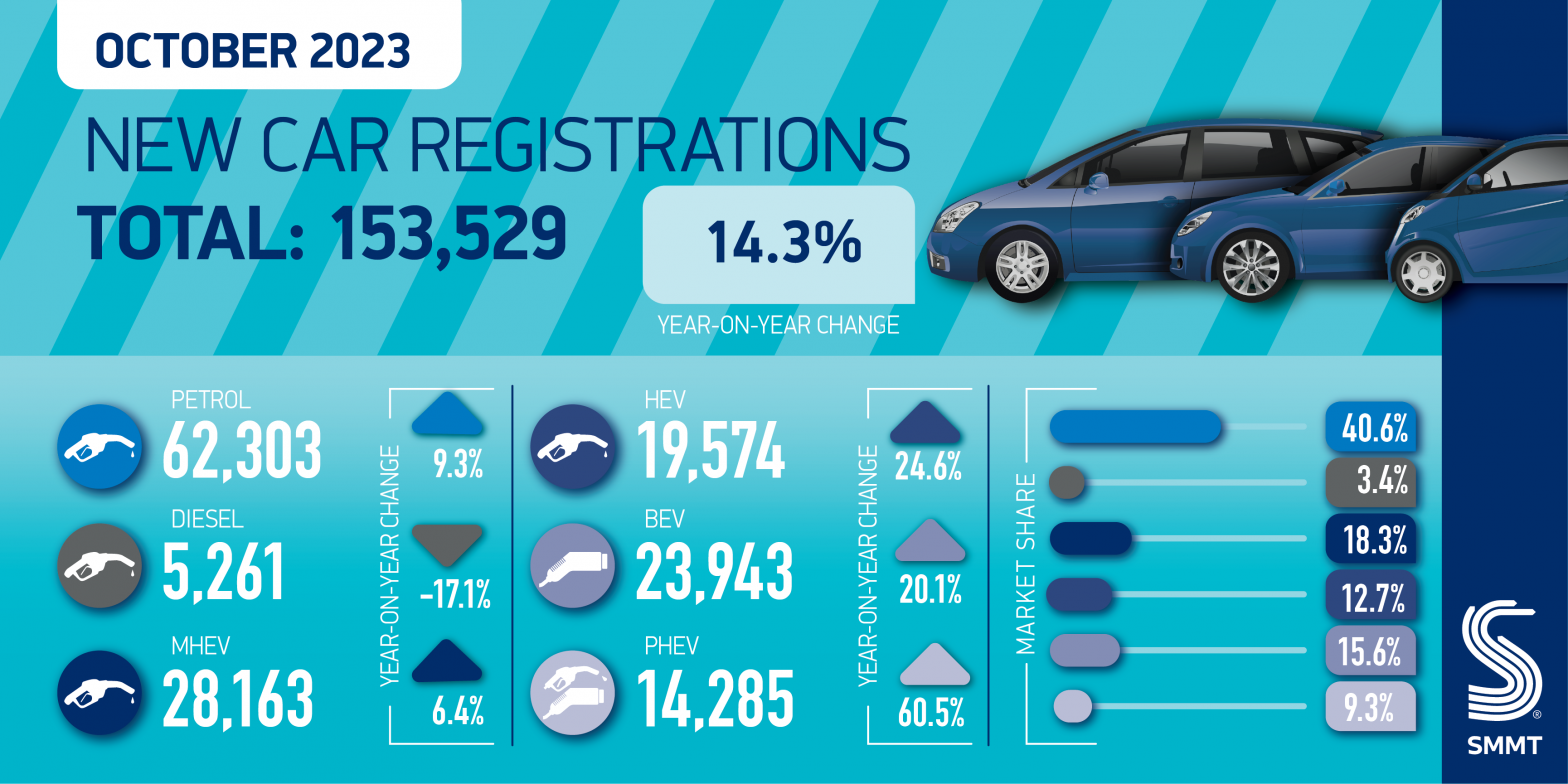

- October delivers 153,529 new car registrations, up 14.3% year-on-year and 7.2% above 2019.

- Battery electric vehicle (BEV) uptake records 42nd consecutive month of growth but struggles to increase market share, while chargepoint rollout improves in efforts to get ahead of need.

- New market outlook revised upwards to 1.886 million units with further growth anticipated in 2024, but BEV uptake expectations downgraded slightly.

SEE CAR REGISTRATIONS BY BRAND

DOWNLOAD PRESS RELEASE AND DATA TABLE

October’s new car market grew by 14.3% to reach 153,529 registrations, 7.2% above pre-pandemic levels and marking the best performance for the month since 2018, 1 according to the latest figures from the Society of Motor Manufacturers and Traders (SMMT). 2

The 15th month of consecutive growth was driven almost entirely by large fleet registrations, which grew 28.8% to reach 87,479 units. Private demand was stable at 62,915 vehicles, a 0.3% increase, while the much smaller business sector saw registrations fall -15.2% to 3,135 units. With the sustained increase in new car registrations, overall vehicle uptake is now up 19.6% in the first 10 months, with the market currently enjoying its best year since 2019.

Electrified vehicle uptake continued to accelerate in October accounting for 37.6% of all new car registrations. Hybrid electric vehicles (HEVs) grew 24.6% to reach 19,574 units, while plug-in hybrid vehicles (PHEVs) recorded the highest proportional growth, up 60.5% to 14,285 registrations. Battery electric vehicle (BEV) uptake increased for the 42nd month in a row, by 20.1% to 23,943 units.3 Given overall market growth, however, this amounted to a BEV market share of 15.6%, a relatively small rise from last year’s 14.8%. Furthermore, private registrations accounted for fewer than one in four new BEVs this year, underscoring the need for fiscal incentives for private consumers.4 Year to date, BEV volumes have risen 34.2% to account for 16.3% of new registrations this year, up slightly from 14.6% this time last year.

October’s plug-in vehicle performance follows a significant increase in chargepoint rollout in Q3, which improved significantly relative to new plug-in car uptake. 4,753 new standard chargepoints came online in the quarter, the largest ever quarterly delivery. This equates to one new standard public chargepoint being installed for every 26 new plug-in cars reaching the road between July and September, improved from 38 in the same quarter last year.5 However, installation was disproportionately focused on London and the South East, which received four out of five new chargepoints commissioned during the quarter – despite the region accounting for fewer than two in five new plug-in registrations during the same period.6 In comparison, just 13 chargers were installed in Yorkshire and Humberside, while the North actually had 105 chargers taken out of service.

With EV uptake greatly influenced by perceptions of chargepoint infrastructure availability and accessibility, action should be taken to ensure more equitable distribution and pricing for public charging. Reducing VAT on public charging to match home use would mean those unable to install their own chargepoint – typically those in flats, terraces and rented accommodation – would avoid paying four times the tax paid by those who can – typically those who own houses with off-street parking. Binding targets for chargepoint rollout, in line with those set for the car market by the Zero Emission Vehicle Mandate and supported by the necessary changes to planning and grid connections so desperately needed, would also help accelerate installation, giving consumers confidence in being able to charge when and where needed.

Mike Hawes, SMMT Chief Executive, said,

With demand for new cars surpassing pre-pandemic levels in the month, the market is defying expectations and driving growth. As fleet uptake flourishes, particularly for EVs, sustained success depends on encouraging all consumers to invest in the latest zero emission vehicles. The Autumn Statement is a key opportunity for government to introduce incentives and facilitate infrastructure investment. Doing so would send a clear signal of support for drivers, reassuring them that now is the time to switch to electric.

The latest market outlook has been revised upwards to reflect market growth higher than expected. Overall new car registrations are anticipated to reach 1.886 million by the end of the year, a rise of 2.1% on July’s expectations. However, expectations for BEV uptake have been downgraded again slightly, by -1.7% to 324,000 units resulting in an expected market share at year end of 17.2%.

Looking ahead to next year, the overall market outlook for 2024 is marginally more positive than previously anticipated, up 1.0% to 1.970 million units (a 4.4% rise on the 2023 outlook). With an absence of consumer incentives and an overwhelming dependency on fleet registrations for growth, however, BEV market share outlook has been revised down slightly to an expected market share of 22.3%, despite registrations expected to reach 439,000 units, a 35.5% increase over 2023.

Notes to editors

1 October 2018: 153,599

2 October 2019: 143,251

3 April 2020: BEV registrations fell -9.7%

4 YTD 2023 BEV registrations: 262,487; Private BEV registrations: 62,478

5 Based on SMMT analysis of new BEV and PHEV registrations

6 Based on SMMT analysis