Ajay Joshi, chemical industry expert, says “in solvent and commodity chemicals, Indian companies would continue to face pressure in terms of pricing, in terms of margins from Chinese chemical companies. The bright spot for the Indian chemical segment would be battery chemicals where the EV ecosystem is developing with newer investments from Tesla, VinFast who are going to set up EV plants in India.”

What are the big trends for the Indian chemical manufacturing sector for 12-18 months?

Ajay Joshi: Talking about the Indian chemical industry, this year agrochemicals will continue to deal with subdued demand. Right now, we are in the rabi crop season and already the wheat sowing is down 1%, oilseeds down 7% and pulses down 5%. Now, 30-35% of agrochemicals in India are consumed during the rabi season and already, we are facing a downturn.

Furthermore, the Latin American market, which is the number one export market for Indian agrochemical companies, is slowing. On the other side, in the US market also, there is an inventory slowdown. So, for agrochemicals, this year will remain similar to last year, also the next 8 to 10 months only towards the end of this calendar year we will see some recovery. Other segments of the Indian chemical industry will continue to face price and margin pressure from China. Just like you talked about that earlier, it used to be China plus one, now it is China 2.0, China’s return.

Last calendar year, January to December 2023, 80 million metric tonnes of new chemical capacities including agrochemicals were added into China. Now, China is having the largest acetic acid capacity, 60% of global acetic acid capacities are in China. For terephthalic acid, they are now number one. From net importer in 2019, China in 2023 became net exporter of terephthalic acid.

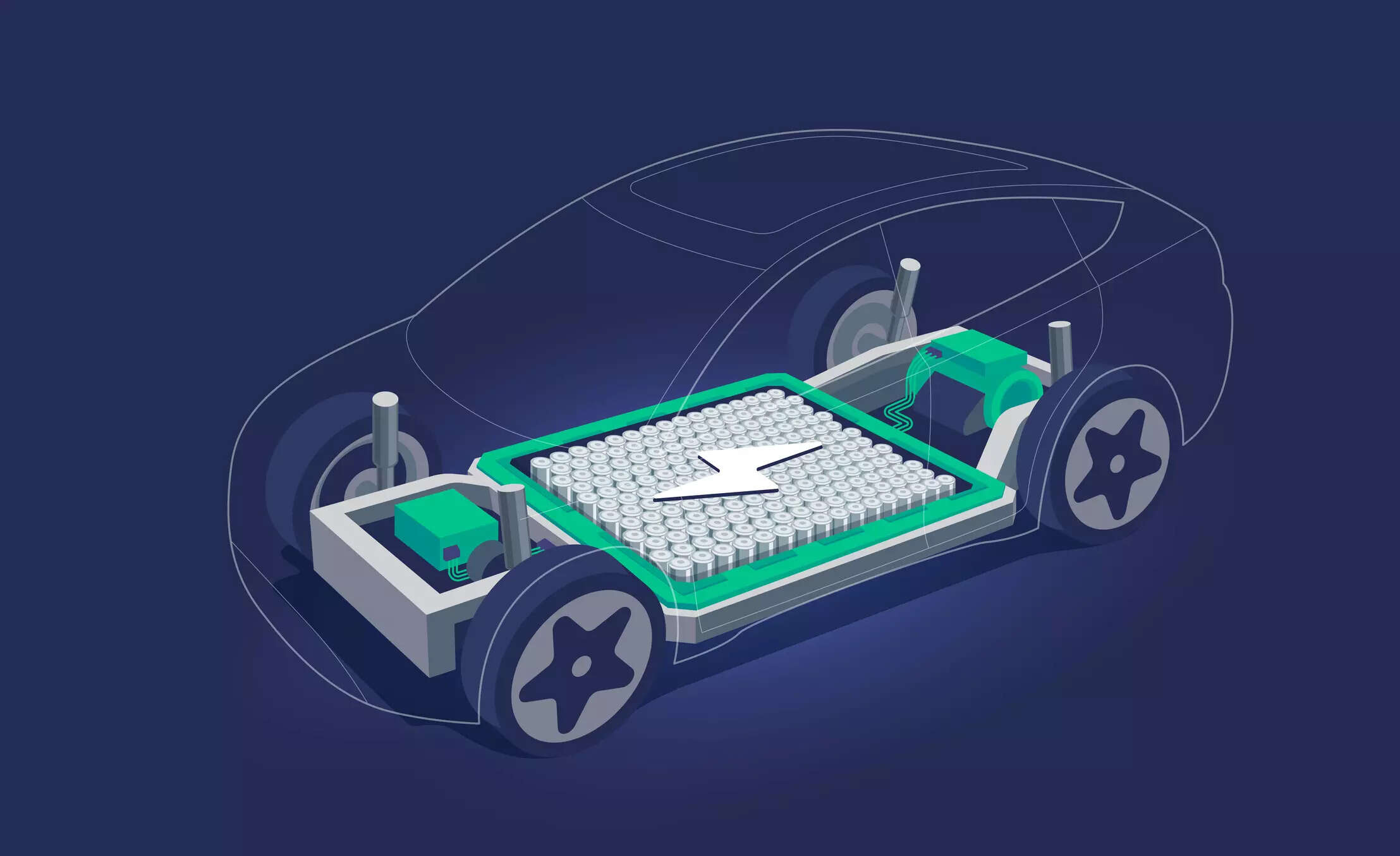

In solvent and commodity chemicals, Indian companies would continue to face pressure in terms of pricing, in terms of margins from Chinese chemical companies. The bright spot for the Indian chemical segment would be battery chemicals where the EV ecosystem is developing with newer investments from Tesla, VinFast who are going to set up EV plants in India.

So, companies planning to enter or already entering the EV battery chemicals space whether it is graphite manufacturer, organometallic salt manufacturers, electrolyte manufacturers, or solvent manufacturers, will see very good outlet sales domestically. Overall, the weaker demand cycle whether it is domestic or global has not turned around yet. The pressure is going to remain from China.

But this quarter, specifically towards the first week of February, China will go for their lunar new year and we will see a slight increase in certain commodities like caustic soda, acetic acid, phenol, caprolactam, mono ethylene glycol. But again, once China resumes towards mid of February, the prices will again go back to the downward side.

But the Chinese lunar year is a regular annual event. Why will it have an impact this year?

Ajay Joshi: Yes. So, this year, the reason is that the demand already, domestic China demand is anyway weak, that is number one thing. Second, in India also, demand is very weak. China exports to Latin America are competing with Indian exporters. So, these are some of the reasons that this trend will take place.

One of the recent up and coming trends has been battery chemicals and that is one space that the Indian companies are looking at garnering more market share of. Which are companies you think have a right to win in this space?

Ajay Joshi: In battery chemicals, in the electrolyte and solvent space, which is the hot cake right now, Aether Industries, AMI Organics, Tatva Chintan, these are some of the companies. In fact, Aether Industries, they also happened to sign an MOU with the leading EV company for a multi-year supply contract of electrolyte.

Apart from that, AMI Organics, Tatva Chintan are also entering the electrolyte solvent space for battery chemicals.

Earlier in India, the demand outlets were not present, similar to China, but now with, like I said, EV companies investing into capacities in India, the demand outlets will open up. So, companies operating in this space will have a very-very demand turn. On the other side, for graphite manufacturers who would supply to the anode part of the batteries, companies like HimadriPhillips Carbon Black, they will also see very-very strong demand.

Agrochemicals sector has been a bit of a worry with respect to the excess inventory; demand has been a little bit subdued as well. Just want to know the road ahead in terms of some of these concerns, what it brings forth.

Ajay Joshi: For India, 55% to 60% of agrochemicals exports happen to the Latin American and US markets. The Latin American demand is very slow plus we are competing with a lot of Chinese suppliers there. In the US market on the other side, the days’ inventory outstanding value for agrochemicals at the stockist is around 70 to 80 days compared to the average of 45 to 50 days. Even the US market is facing a slowdown.

So, the orders will be pushed forward for a lot of Indian agrochemical exporters. On the other hand the capacity additions in China, particularly pyroxasulfone alone, the demand for this molecule is around 3800 metric tonnes. On the other hand, China added two new capacities, adding to 4000 metric tonnes per annum for pyroxasulfone alone. Similarly, new capacities have been added for 2,4-D, glucosinolates, metconazole, and so many other products. So, Indian players would continue to face fierce competition from the Chinese even in export markets, while the domestic demand is already slowing.

We are a financial channel. People want to hear and connect the dots here. If you are an investor, would you buy chemical stocks? If yes, which are the ones you will buy? Purely based on not the price, purely based on the earnings, where you think they are headed.

Ajay Joshi: Right now, some of the companies from the investor point of view we need to look forward to what is the order book plus what are the growth segments. Agrochemicals definitely is not a segment to enter into right now because for the next 8 to 12 months also there will not be any turnaround. But companies active in the speciality chemicals space and contract manufacturing space where we have visible order book, like Anupam Rasayan, Aarti Industries, Aether Industries, these are some of the companies where investors should look forward to in terms of buying.

Where do you think Europe will be because, the (9:08) BASFs and perhaps the bears of the world, they do have a huge advantage of manufacturing and technology because of their headquarters based out of Europe. Could that be a deciding factor for agrochemicals?

Ajay Joshi: For agrochemicals, in particular, if you look at the BASFs of the world, they already are doing asset transfer to China. Now, agrochemicals also will be carved out as a separate entity in India also. That means that in India also, (9:37) agrochemicals will have newer investment because it will have autonomy to operate. Europe will not play a major factor in 2024 because they already are struggling with higher production costs because of the Russia-Ukraine situation, so they are doing asset transfer to China. They are setting up big-scale plants in China. If I talk about (9:56) of the world, all the European majors. So, from Europe’s side, even the domestic demand is also going to remain weak and the chemical output is also going to remain flattish.

Which is the other up-and-coming space that you would want to watch out for that, apart from the battery subset that we discussed, whether oleochemicals, whether the other subsets, what looks interesting as a theme now?

Ajay Joshi: Fluoropolymers. Companies like Anupam Rasayan, Navin Fluorine, GFL, these companies are going to have a party because Japan and Korea, they are looking at India only as a supply partner, not China because of their trade issues and other geopolitical issues. In fact, Anupam Rasayan, although it was a late entrant into fluoropolymers business, it is getting huge MOUs and forward contracts. Similarly, Navin Fluorine is also working on newer molecules for lithium and battery casing which requires fluoropolymers. Now, these are very high-margin, high-value niche applications. So, fluoropolymers is going to remain another space to look forward to.