India’s electric vehicle (EV) industry wrapped up CY2023 on a strong note with total retails surpassing 1.53 million units, an increase of 49% over CY2022’s 1.02 million units. The past two years have been particularly good for the sector as OEMs benefit from the growing consumer shift to e-mobility while EV buyers gain from the larger number of EVs across the two- and three-wheeler and passenger vehicle segments.

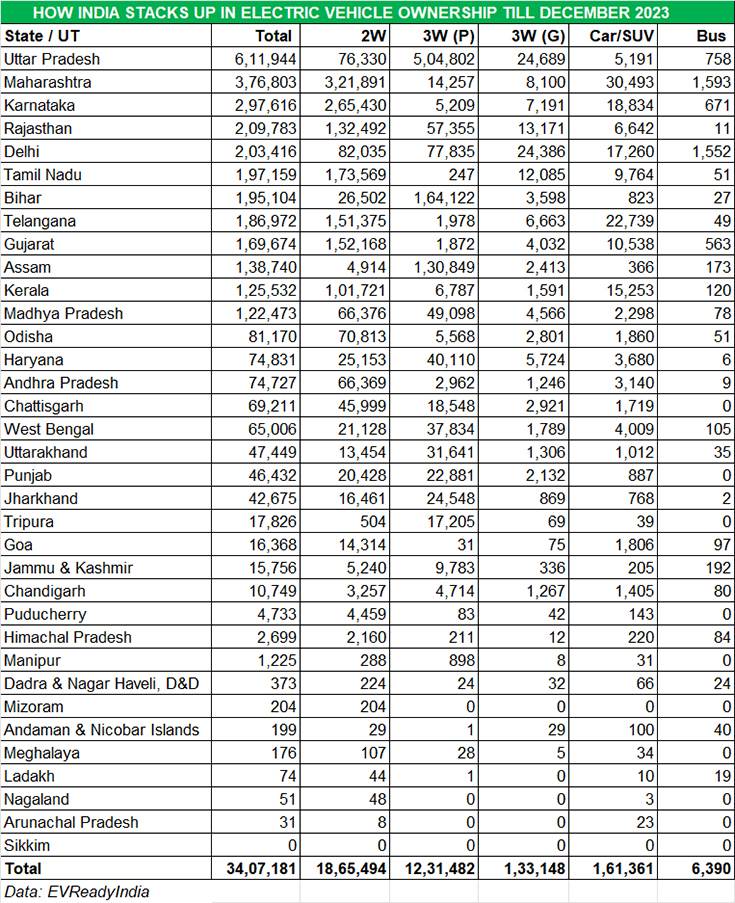

Cumulative 10-year retail data from the government’s Vahan portal reveals that India EV Inc has seen sales grow from a very low 2,390 units in CY20214 to 15,31,177 units in CY2023 (see data table below).

Given the growing market size of the domestic EV industry, it is interesting to delve into data to find out just how EV ownership / EV population stacks up across India. A deep dive into just where the 3.4-plus million EVs have been bought and are plying on Indian roads reveals some interesting trends.

EV sales in CY2023 achieved a new high – 1.53 million units.

EV sales in CY2023 achieved a new high – 1.53 million units.

ELECTRIC 2- AND 3-WHEELERS HAVE 95% OF INDIA EV MARKET

India EV Inc’s strong growth trajectory has its footprint across multiple states and Union territories in terms of EV ownership. With nearly all States and Union Territories wooing EV buyers with EV-ownership friendly policies and measures, finding out how they fare on the EV ownership / user chart is important. A deep dive into the EVreadyIndia dashboard, which consolidates sales data for all 34 Vahan states and Union Territories, and also Telangana, till end-December 2023, provides some interesting takeaways.

Given their level of affordability, the electric two- and three-wheeler sub-segments will always be the volume drivers. Of the total EV population of 3.40 million units (34,07,181 units as of end-December 2023), 1.86 million or 54.75% comprise electric scooters and motorcycles. Then there are 1.36 million three-wheeler owners, comprising both passenger-carrying and cargo carriers and accounting for 40.05% of the overall market. Club the two and what you get is 94.80% of the India EV market, leaving the balance to electric passenger vehicles (1,61,361 units / 4.73% share), electric buses (6,390units / 0.18% share) and others (9,306 units, likely electric cargo vehicles).

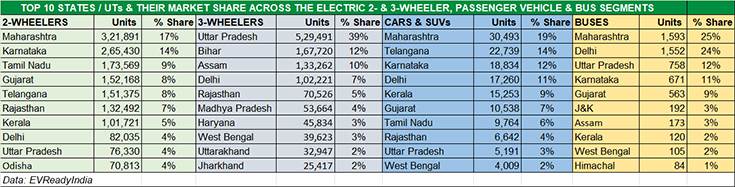

UTTAR PRADESH, MAHARASHTRA & KARNATAKA TOP 3 STATES IN EV OWNERSHIP

Uttar Pradesh has the largest number of EVs – 529,680 units – mainly because it has the largest number of electric three-wheelers – 463,393 units. Maharashtra with 320,189 EVs, however, tops in e-two-wheelers, e-passenger vehicles as well as e-buses.

Uttar Pradesh has the largest number of EVs – 529,680 units – mainly because it has the largest number of electric three-wheelers – 463,393 units. Maharashtra with 320,189 EVs, however, tops in e-two-wheelers, e-passenger vehicles as well as e-buses.

India EV Inc’s strong growth trajectory has its footprint across multiple states and Union territories in terms of EV ownership. With nearly all States and Union Territories wooing EV buyers with EV-ownership friendly policies and measures, finding out how they fare on the EV ownership / user chart is important.

As per the data, of the total 34,07,181 EVs sold in India till end-December 2023, 12 states including one UT, each with six-figure sales, cumulatively account for 28,35,216 EVs or 83.21 percent. The top three states – Uttar Pradesh, Maharashtra and Karnataka – together account for 12,86,363 EVs or 37.75% of the India total.

Uttar Pradesh (UP) is the state with the largest number of EVs – 6,11,944 units and commands 18% of the total EV parc in India. This is thanks to UP being the state with the largest number of electric three-wheelers – 529,491 units and an overwhelming 39% of the 1.36 million three-wheeler sales in India.

In the other e-sub-segments, Uttar Pradesh ranks down the line – in e-two-wheelers, the state is in ninth position with 76,330 units (4% e2W market share), and also ninth in e-passenger vehicles (5,191 units / 4% ePV market share) and third in e-buses (758 units / 12% market share).

Maharashtra is ranked second overall on the all-India EV ownership scale with 376,803 units and an 11% share. However, it has the bragging rights because it is the leader in e-two-wheelers, electric cars and SUVs, and also e-buses. Of the 1.86 million e-two-wheelers sold in India till end-December 2023, Maharashtra with 321,891 units has the largest share of 17.25 percent. Likewise, in e-PVs, the state leads with 30,493 units or 19% of the 161,361 cars and SUVs sold till September 2023. And in e-buses, Maharashtra tops with 1,593 units and a 25% market share, just ahead of Delhi which has a 24% share.

Karnataka, with 2,97,616units and 8.73% of India EV sales till end-December 2023, is the overall No. 3 as a result of its second rank in e-two-wheelers (265,430 units / 14% share), third rank in e-PVs (18,834 units / 12% share) and fifth rank in e-buses (671 units / 11% share). The state is low down the order in e-three-wheelers – 12,400 units across both passenger and cargo models.

Rajasthan, with 209,783 units, takes fourth position in EV sales in India, and is ahead of Delhi by 6,367 units. The bulk of its sales comprise e-two-wheelers (132,492 units / 7% share). While the state’s e-three-wheeler parc is 70,526 units (5% share), its residents have also bought 6,642 e-PVs (4% share).

Delhi, with 2,03,416 units, is ranked fifth on the all-India chart. The largest segment-wise EV population in India’s capital city is that of three-wheelers – 102,221 units (77,835 passenger e3ws and 24,386 cargo e3Ws), where it ranks fourth after UP, Bihar and Assam. The capital city is also home to 82,035 two-wheelers, 17,260 e-PVs and is just behind Maharashtra with 1,552 electric buses plying on its roads.

Tamil Nadu, which aims to become the EV hub of the country and has recently bagged Vietnamese EV maker VinFast’s mega investment for setting up an integrated EV plant in Thoothukud, has seen sales of 197,159 EVs which includes 173,569 e-two-wheelers and a 9% all-India share, ranking third after Maharashtra (321,891 e2Ws) and Karnataka (265,430 e2Ws). Tamil Nadu is seventh on the e-passenger vehicle table with 9,764 units and a 6% all-India share.

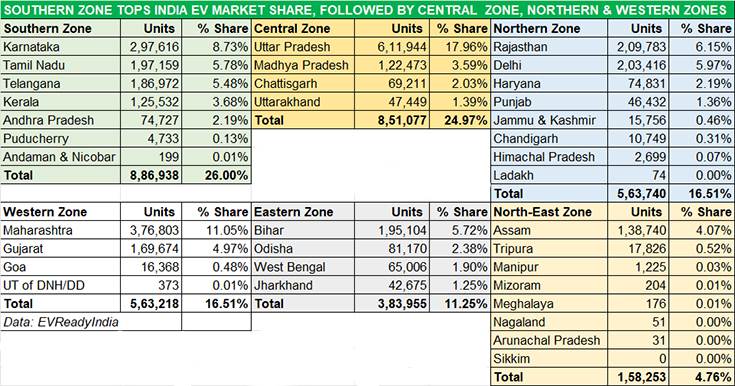

SOUTHERN ZONE WITH 886,938 UNITS & 26% SHARE TOPS EV PARC

Southern India is increasingly where the EV action is what with Karnataka, Tamil Nadu, Telangana and Andhra Pradesh housing the manufacturing operations of the leading two-wheeler OEMs ranging from e-three-wheeler market leader Mahindra Last Mile Mobility’s plant in Bengaluru to Ather Energy’s state-of-the-art 420,000-units-per-annum facility at Hosur, Tamil Nadu or Hero MotoCorp’s Vida-producing factory at Chittoor in Andhra Pradesh.

Southern India is increasingly where the EV action is what with Karnataka, Tamil Nadu, Telangana and Andhra Pradesh housing the manufacturing operations of the leading two-wheeler OEMs ranging from e-three-wheeler market leader Mahindra Last Mile Mobility’s plant in Bengaluru to Ather Energy’s state-of-the-art 420,000-units-per-annum facility at Hosur, Tamil Nadu or Hero MotoCorp’s Vida-producing factory at Chittoor in Andhra Pradesh.

Cumulatively, along with Kerala, the five states and two UTs account for 886,938 EVs or a leading 26% share of the total Indian EV market.

Tamil Nadu has already made its intention clear to become the EV capital of the country and given the momentum and the sharpened focus of Southern India, expect this region to continue to provide the fireworks when it comes to increasing EV ownership.

The Southern Zone though has a challenger in the Central Zone, which is just 35,861 EVs behind. A cumulative EV population of 851,077 units across the states of Uttar Pradesh, Madhya Pradesh, Chattisgarh and Uttarakhand gives this zone a 24.97% share of the all-India EV market. This is because of the dominant presence of Uttar Pradesh (611,944 units) which is the leader in e-three-wheelers with 529,491 units, which account for 87% of its total EV sales. Uttarakhand, with 47,449 units, is ranked 18th in the overall India ranking. Expect the Central Zone to continue to be dominated by the demand for electric three-wheelers for inter-city people transportation as well as growing ownership of last-mile mobility two- and three-wheelers.

NORTHERN AND WESTERN ZONE HAVE SIMILAR 16.51% EV SHARE

The Northern Zone and Western Zone, both of which have an EV parc of over half-a-million units, are separated by just 522 units! At 563,740 EVs, the Northern Zone has a 16.51% share of India EV market, just like the Western Zone. This region is led by Rajasthan (209,783 EVs), Delhi (203,416 EVs) and Haryana (74,831 EVs). The northern region, particularly Delhi, Rajasthan and Haryana, is home to the bulk of the nearly 450 three-wheeler manufacturers in the country as well houses the plants of Hero Electric and Okinawa Autotech. This region, as has been recorded for the past few years, continues to see poor levels of AQI (Air Quality Index), which is also a driver of demand for zero-emission, eco-friendly EVs.

The Western Zone, comprising of two key markets in Maharashtra and Gujarat, along with Goa and the Union Territory of Dadra and Nagar Naveli, and Diu and Daman, have a total of 563,218 EVs. This gives the region a 16.51% share in the overall India market, fourth after the Southern, Central and Northern zones.

Thanks to its leadership in two-wheelers, e-PVs and e-buses, Maharashtra is the No. 2 state volume-wise for EV ownership in the country after Uttar Pradesh. In the state-wise listing within the Western Zone, Maharashtra with 376,803 units and 11% state share is followed by Gujarat (169,674 units / 5% state share), Goa (16,368 units) and the UT of Dadra & Nagar Haveli, Daman & Diu (373 units).

The Eastern Zone is close to the 400,000 EV parc with 383,955 units, most of them in Bihar (195,104 units), followed by Odisha (81,170 units), West Bengal (65,006 units) and Jharkhand (42,675 units).

Meanwhile, the North-Eastern Zone, which comprises all of eight states, has 158,253 EV users and accounts for a 4.76% share of the India EV market. Leading them is Assam with 138,740 units, which is ranked 10th on the all-India list.

INDIA EV INDUSTRY FIRMLY PLUGGED INTO GROWTH MODE

What is helping accelerate EV ownership in India is a combination of factors. While demand for e-mobility was tepid in the initial years of the past decade, the government’s heightened focus towards the EV sector and the overall electric mobility eco-system in the form of the FAME Scheme and PLI (Production-Linked Incentive) Scheme for the automotive sector, along with EV OEMs across vehicle segments expanding their portfolio, and component suppliers either developing in-house or sourcing the latest e-powertrain and parts technologies have all contributed towards the sector’s growth.

Furthermore, growing consumer awareness of the need for eco-friendly mobility amidst the damaging effects of climate change which has also impacted India is helping the cause of EVs. Also, given the high prices of fossil fuels like petrol and diesel, and also CNG, the wallet-friendly nature of EV cost of ownership over the long run is a big catalyst for consumers planning to transition from IC engine motoring to EVs.

Another catalyst is the EV-friendly policies. Most of the states and UTs have notified EV policies which deliver plentiful benefits to EV uses and help accelerate the pace of EV adoption across the country.

Given the rapid pace of growth, the Indian EV industry can be expected to notch consistent progress. The EV-Ready India dashboard has forecast 45.5% CAGR in EVs between 2022 and 2030, rising to annual sales of 1.6 crore EVs in India by 2030. Some challenges remain like inadequate charging infrastructure and high initial EV prices, which is directly related to the battery cost. Nevertheless, with both the private and public sectors aggressively investing heavily in expanding the charging network across India, range anxiety for EV users should reduce over the coming years.

There is also the sharpened focus from OEMs and component suppliers on localisation with a view to reduce costs and enhance affordability, and battery prices expected to reduce gradually, industry is optimistic about growth for this eco-friendly form of mobility, both in the near-term and long-term.

In CY2023, EVs accounted for 6.38% of overall automobile retail sales in India, up from 5% in CY2022. Vehicle manufacturers and captains of industry are always cued into consumer buying trends. This analysis of all-India EV ownership or EV population offers many a cue to just where the EV action currently lies in the country and for which sub-segment of the sector.