As the first-quarter 2024 earnings season for the auto sector draws to a close, a mixed picture is emerging. Per the Earnings Trends report dated May 8, the beat ratio for the bottom line was 62.5%, while the same for the top line was 50%. While overall earnings of the sector have declined 19% year over year amid macroeconomic uncertainty due to inflationary pressures and geopolitical tensions, there is still some optimism left.

A few prominent players in the industry — General Motors GM, BorgWarner BWA, and Oshkosh Corp. OSK — have defied the pessimism and uncertainty by upwardly revising their guidance.

The raised guidance not only shows the companies’ confidence in their prospects but also attracts investors looking for promising opportunities. However, are these upward forecasts enough to consider investing in these auto stocks? Let’s delve deeper.

General Motors: The U.S. auto giant reported first-quarter 2024 adjusted earnings of $2.62 per share, which surpassed the Zacks Consensus Estimate of $2.08 and increased 18.5% year over year. Revenues of $43.01 billion beat the Zacks Consensus Estimate of $41.28 billion and increased from $39.9 billion recorded in the year-ago period.

On the back of encouraging first-quarter performance, GMNA market strength, cost-reduction efforts, and focus on improving EV business sales and profitability, the company has lifted 2024 forecasts. GM now expects adjusted EBIT in the range of $12.5-$14.5 billion, up from $12-$14 billion guided earlier. Adjusted EPS is anticipated in the range of $9-$10, up from $8.50-$9.50, guided earlier. Adjusted automotive free cash flow is expected in the band of $8.5-$10.5 billion, higher than the prior forecast of $8-$10 billion.

General Motors’ superior liquidity profile (total automotive liquidity of $33.3 billion as of Mar 31, 2024) and investor-friendly moves also instill confidence. In the last reported quarter, GM bought back around 13 million shares, including 4 million from the accelerated share repurchase program. The company’s first-quarter dividend also marked a 33% hike.

While stiff competition (especially in China market) and high R&D costs and capex requirements are somewhat concerning, we think that the positives are set to outweigh the near-term hiccups. You can consider parking your money in the stock. Also, the legacy automaker is attractively valued. It is trading at a forward sales multiple of 0.29, below its median of 0.35 over the last five years.

Image Source: Zacks Investment Research

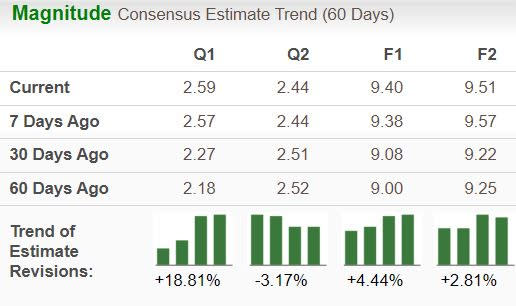

Analysts have upwardly revised GM’s earnings outlook for the current fiscal. Over the past seven days, EPS estimates for 2024 have moved up by 2 cents to $9.40, implying 22.4% growth year over year. General Motors currently carries a Zacks Rank #3 (Hold) and has a Value Score of A.

Image Source: Zacks Investment Research

Oshkosh: This automotive equipment provider reported first-quarter 2024 adjusted earnings of $2.89 per share, beating the consensus mark of $2.26 and rising from $1.59 per share recorded in the year-ago period. Consolidated net sales climbed 12.2% year over year to $2.54 billion. The top line also surpassed the Zacks Consensus Estimate of $2.51 billion.

Encouraged by strong first-quarter results, healthy demand for products, solid business execution across segments, launch of innovative offerings, capacity expansions and acquisition synergies, OSK raised its 2024 guidance. Oshkosh now expects consolidated 2024 sales, adjusted operating income and adjusted EPS to be around $10.7 billion, $1.075 billion and $11.25, up from previous projections of $10.4 billion, $990 million and $10.25, respectively. For the second quarter, Oshkosh expects adjusted EPS to be around $3 per share, up sequentially and year over year. It expects sales to be up approximately 15% versus the prior year.

The firm’s balance sheet strength and investor-friendly moves also spark confidence. The total debt-to-capital ratio stands at 0.13, lower both in absolute and relative terms. In 2023, it hiked its dividend by 12.2%, which marked the tenth consecutive year of double-digit percentage increase.

In the first quarter of 2024, Oshkosh repurchased nearly 130,000 shares of common stock worth $15 million.Additionally, the robust consolidated backlog of $16.35 billion provides enough visibility for the coming years. OSK also trades at a discount compared to the broader industry. It is trading at a forward sales multiple of 0.75, way below its high of 1.18 over the last five years. Considering all the factors, we are bullish on the stock.

Image Source: Zacks Investment Research

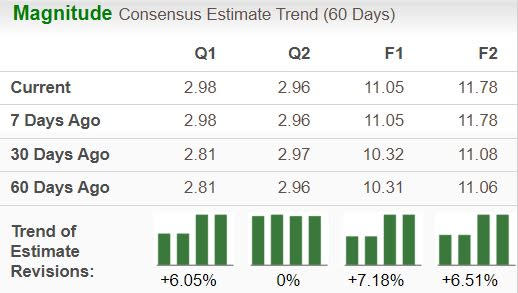

Analysts have upwardly revised OSK’s earnings outlook for the current fiscal. Over the past 30 days, EPS estimates for 2024 have moved up by 73 cents to $11.05, implying 10.7% growth year over year. Oshkosh currently carries a Zacks Rank #1 (Strong Buy) and a Value Score of B.

Image Source: Zacks Investment Research

BorgWarner: This automotive parts supplier reported adjusted earnings of $1.03 per share for first-quarter 2024, down 5.5% year over year but surpassed the Zacks Consensus Estimate of 87 cents. Net sales of $3.6 billion declined 13.9% year over year but beat the Zacks Consensus Estimate of $3.52 billion.

BWA has raised its full-year EPS guidance. Adjusted EPS is now expected to be within a range of $3.80-$4.15, up from $3.65 to $4.00 guided earlier. While it reaffirmed sales forecast, the metric is expected to be between $14.4 billion to $14.9 billion, suggesting growth from $14.2 billion recorded in 2023. Frequent business wins are expected to drive top-line growth.BorgWarner’s Charging Forward project to accelerate its electrification strategy bodes well. BorgWarner expects its 2024 eProduct sales in the band of $2.5-$2.8 billion, implying year-over-year growth of 25-40%, with high demand for battery systems being the main driver.

BWA’s manageable leverage and high liquidity are other positives. At the end of the first quarter of 2024, its long-term debt ratio was 0.35, improving from 0.38 at the end of 2023. Also, BorgWarner remains committed to maximizing shareholders’ value.

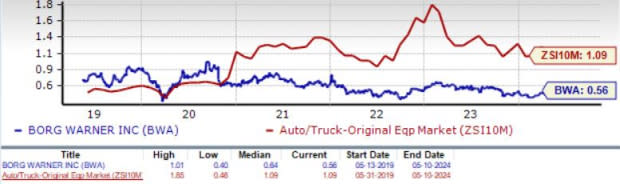

Along with its earnings release, the company also authorized an additional $500 million stock repurchase to be executed over the next three years. While the expected decline in light and commercial vehicle production could decelerate BorgWarner’s organic growth rate in the near term, there are several positives about BorgWarner that lead us to believe in its long-term prospects. BWA is valued at a discount compared to the broader industry. It is trading at a forward sales multiple of 0.56, below its median of 0.64 over the last five years.

Image Source: Zacks Investment Research

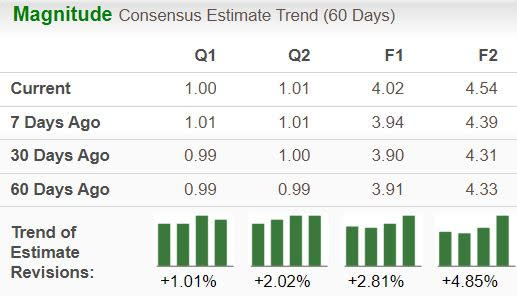

Analysts have also upwardly revised BWA’s earnings outlook for the current fiscal. Over the past seven days, EPS estimates for 2024 have moved up by 8 cents to $4.02, implying 7.2% growth year over year. BorgWarner currently carries a Zacks Rank #1 and has a Value Score of A.

Image Source: Zacks Investment Research

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BorgWarner Inc. (BWA) : Free Stock Analysis Report

General Motors Company (GM) : Free Stock Analysis Report

Oshkosh Corporation (OSK) : Free Stock Analysis Report