Amid a backdrop of fluctuating global markets, the Hong Kong stock market has experienced its share of volatility, recently marked by a notable 2.84% drop in the Hang Seng Index. In such an environment, investors might find reassurance in companies with high insider ownership, suggesting a strong alignment between company management and shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

iDreamSky Technology Holdings (SEHK:1119) |

20.1% |

104.1% |

|

New Horizon Health (SEHK:6606) |

16.6% |

62.3% |

|

Fenbi (SEHK:2469) |

32.1% |

43% |

|

Meitu (SEHK:1357) |

38% |

33.7% |

|

DPC Dash (SEHK:1405) |

38.2% |

89.7% |

|

Adicon Holdings (SEHK:9860) |

22.3% |

29.6% |

|

Zylox-Tonbridge Medical Technology (SEHK:2190) |

18.5% |

79.3% |

|

Beijing Airdoc Technology (SEHK:2251) |

27.4% |

83.9% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

100.1% |

|

Ocumension Therapeutics (SEHK:1477) |

17.7% |

93.7% |

We’re going to check out a few of the best picks from our screener tool.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited operates in the automobile and battery sectors across China, Hong Kong, Macau, Taiwan, and internationally, with a market capitalization of approximately HK$717.78 billion.

Operations: The company generates revenue primarily from its automobile and battery sectors.

Insider Ownership: 30.1%

BYD, a prominent player in Hong Kong’s growth-oriented sectors with significant insider ownership, recently expanded its global footprint by launching the BYD SHARK pickup in Mexico, marking its first major product introduction outside China. This move aligns with BYD’s robust sales growth, as evidenced by a substantial year-over-year increase in unit sales reported in April 2024. Despite not being the top example of high insider ownership growth companies, BYD continues to show strong market expansion and innovation capabilities. The company also demonstrated financial strength with increased net income and revenue in Q1 2024 compared to the previous year.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: China Ruyi Holdings Limited operates as an investment holding company focused on content production and online streaming, serving markets in the People’s Republic of China, Hong Kong, Europe, and internationally, with a market capitalization of approximately HK$25.74 billion.

Operations: The company generates revenue primarily through its content production business, which earned CN¥2.23 billion, and its online streaming and gaming segments, which together brought in CN¥1.38 billion.

Insider Ownership: 15.3%

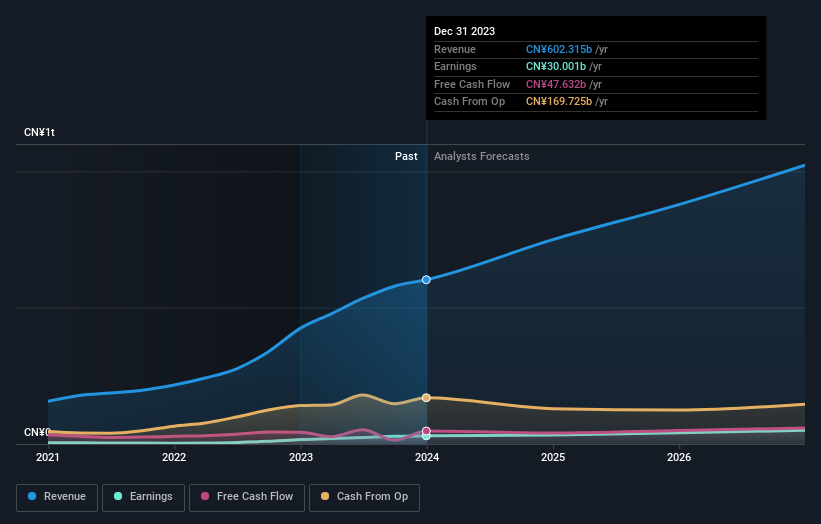

China Ruyi Holdings, while not the pinnacle of growth companies with high insider ownership in Hong Kong, shows a promising trajectory with its recent significant earnings and revenue upsurge. In 2023, the company’s sales more than doubled to CNY 3.63 billion from CNY 1.32 billion, although net income slightly decreased to CNY 689.76 million from CNY 789.53 million year-over-year. The firm is trading at a substantial discount against its estimated fair value and forecasts indicate robust annual revenue growth at 27.7%, outpacing the Hong Kong market’s average of 7.9%. However, concerns linger due to lower profit margins compared to the previous year and large one-off items impacting financial results.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Alibaba Health Information Technology Limited operates as an investment holding company, focusing on pharmaceutical direct sales, e-commerce platforms, and healthcare and digital services in Mainland China and Hong Kong, with a market capitalization of approximately HK$55.64 billion.

Operations: The company’s revenue from the distribution and development of pharmaceutical and healthcare business totals CN¥27.03 billion.

Insider Ownership: 24.2%

Alibaba Health Information Technology has demonstrated solid growth, with earnings increasing by 65.6% last year and forecasts predicting a 23.1% annual growth rate. However, shareholder dilution occurred over the past year, and one-off items have affected the quality of earnings. Despite these challenges, the company’s stock is trading at a significant discount to its estimated fair value. Recent developments include a new software services agreement expected to enhance e-commerce operations on Tmall platforms, potentially boosting future revenue streams.

Where To Now?

Curious About Other Options?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1211 SEHK:136SEHK:241.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com