As global markets show signs of resilience and recovery, particularly in the U.S. and China, the Hong Kong market has also experienced a positive uptick, with the Hang Seng Index gaining 1.99% recently. Against this backdrop, insider ownership can be a crucial indicator of confidence in a company’s future performance. In today’s article, we explore three growth companies listed on the SEHK that boast high insider ownership and have reported earnings growth of up to 70%. Understanding these factors can provide valuable insights into potential investment opportunities amidst current market conditions.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

iDreamSky Technology Holdings (SEHK:1119) |

18.8% |

104.1% |

|

Pacific Textiles Holdings (SEHK:1382) |

11.2% |

37.7% |

|

Tian Tu Capital (SEHK:1973) |

34% |

70.5% |

|

Adicon Holdings (SEHK:9860) |

22.4% |

28.3% |

|

Zylox-Tonbridge Medical Technology (SEHK:2190) |

18.7% |

79.3% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

100.1% |

|

Value Partners Group (SEHK:806) |

23.4% |

59.5% |

|

Beijing Airdoc Technology (SEHK:2251) |

28.6% |

83.9% |

|

Beijing Fourth Paradigm Technology (SEHK:6682) |

22.8% |

104.5% |

|

DPC Dash (SEHK:1405) |

38.2% |

91.5% |

Let’s dive into some prime choices out of the screener.

Simply Wall St Growth Rating: ★★★★☆☆

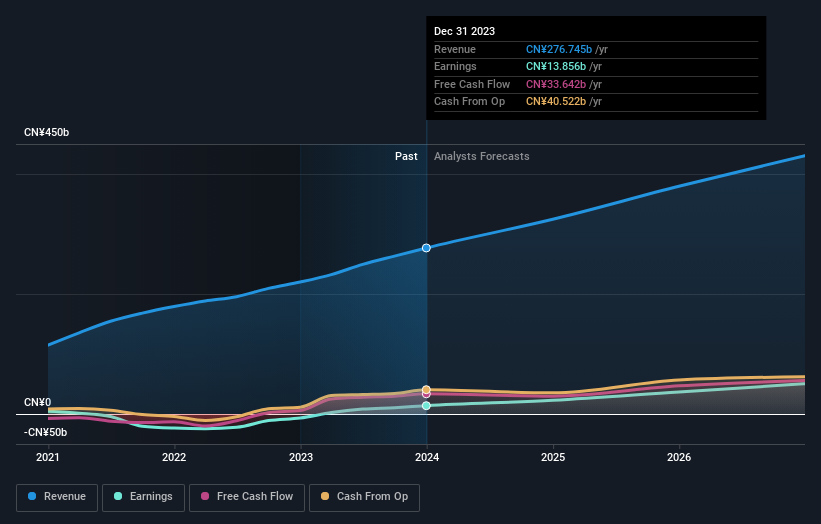

Overview: BYD Company Limited, with a market cap of HK$705.43 billion, operates in the automobiles and batteries sectors across China, Hong Kong, Macau, Taiwan, and internationally.

Operations: BYD’s revenue segments (in millions of CN¥) are derived from its automobiles and batteries business in the People’s Republic of China, Hong Kong, Macau, Taiwan, and internationally.

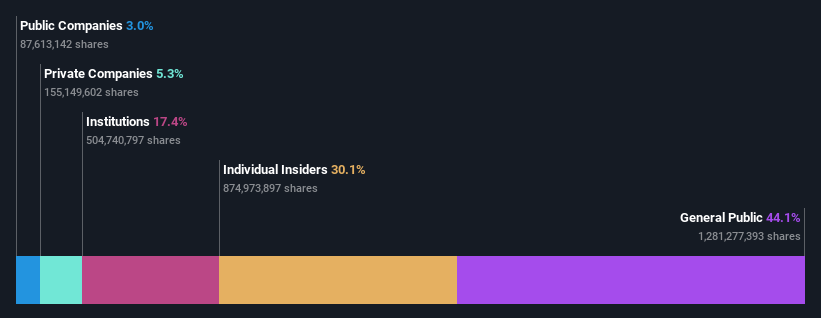

Insider Ownership: 30.1%

Earnings Growth Forecast: 15.2% p.a.

BYD’s recent strategic alliance with Uber, aiming to deploy 100,000 electric vehicles globally, underscores its growth potential. The company’s production and sales volumes have shown substantial year-over-year increases, reflecting robust demand. Additionally, BYD’s inauguration of a new plant in Thailand and the milestone of producing its 8 millionth new energy vehicle highlight its expansion efforts. With revenue growth forecasted at 14% annually and earnings expected to grow faster than the market average at 15.22%, BYD remains a key player in Hong Kong’s growth sector with significant insider ownership.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Tian Tu Capital Co., Ltd. is a private equity and venture capital firm that invests in small and medium-sized companies across early-stage, mature, and pre-IPO stages, with a market cap of HK$2.15 billion.

Operations: The firm’s revenue from Asset Management is -CN¥744.05 million.

Insider Ownership: 34%

Earnings Growth Forecast: 70.5% p.a.

Tian Tu Capital, trading significantly below its estimated fair value, is forecast to achieve substantial revenue growth of 62.7% annually and become profitable within three years. Despite a current net loss due to investment portfolio declines, the company’s earnings are expected to grow by 70.47% per year. However, it has experienced high share price volatility recently and maintains low Return on Equity forecasts at 6.5%.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Meituan operates as a technology retail company in the People’s Republic of China with a market cap of approximately HK$661.07 billion.

Operations: Meituan generates revenue from three main segments: food delivery, in-store, hotel & travel services, and new initiatives & others.

Insider Ownership: 11.6%

Earnings Growth Forecast: 31.3% p.a.

Meituan, trading at 73.1% below its estimated fair value, has seen earnings grow by a very large margin over the past year and is forecast to achieve annual earnings growth of 31.3%, outpacing the Hong Kong market’s average. Despite low insider buying recently, Meituan’s revenue is expected to grow faster than the market at 12.8% annually. Recent changes include amendments to company bylaws and a $2 billion share repurchase program initiated in June 2024.

Next Steps

Searching for a Fresh Perspective?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1211 SEHK:1973 and SEHK:3690.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com