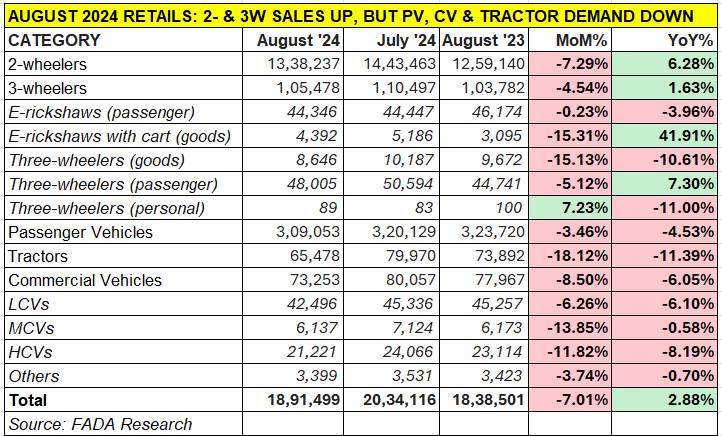

The retail sales numbers and the real-world marketplace report card for India Auto Inc’s performance in August 2024 is out with the Federation of Automobile Dealers Associations (FADA) releasing the data. A total of 1.89 million units were sold, which makes for a 2.88% year-on-year increase (August 2023: 1.83 million units) but is down a substantial 7% month on month (July 2024: 2.03 million units).

Commenting on the sales for last month, FADA president Manish Raj Singhania said: “In August, India witnessed 15.9% excess rainfall across the country, with northwest India seeing a surplus of 31.4%, 7.2% in the east and northeast, 17.2% in central India and a minor deficiency of 1.3% in the peninsular region. This monsoon season brought unpredictable weather, starting with extreme heat waves which delayed monsoon and transitioned into heavy rainfall, leading to flood-like conditions in several areas. These weather anomalies have had a direct impact on India’s auto retail market, which registered a modest YoY growth of just 2.88% in August. While the two-wheeler (2W) and three-wheeler (3W) segments managed to post growth at 6.28% and 1.63%, respectively, other categories faced significant setbacks. Passenger vehicle (PV) sales declined by 4.53%, tractor sales dropped by 11.39% and commercial vehicles (CV) saw a 6.05% drop, underscoring the challenges the industry is grappling with, due to these volatile conditions.”

2-WHEELERS: 1.33 million units, up 6.28% YoY, down 7.29% MoM

2-WHEELERS: 1.33 million units, up 6.28% YoY, down 7.29% MoM

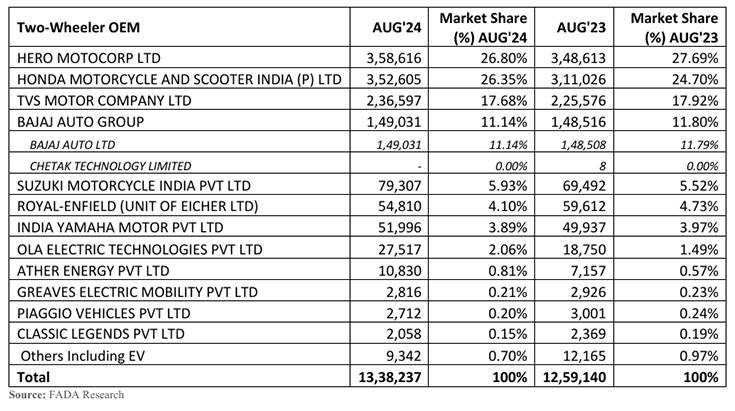

Hero MotoCorp sells 6,011 units more than Honda, market share gap now just 0.45%

The biggest volume segment sold 1.33 million units, up 6% on the 1.25 million units sold a year ago but its August wholesales are 105,226 units lesser than July 2024’s 14,43,463 units (up 17% on July 2023) and down 7% month on month.

FADA pins this down to excessive rain and flooding, which disrupted demand across various regions. In its statement, the dealer body said: “Many customers postponed their purchases, anticipating new product launches, while others deferred due to market saturation and changing preferences. Limited marketing efforts from OEMs and subdued market sentiment further impacted sales. Despite these headwinds, the 2W segment grew by 6.28% YoY, thanks to improved stock availability and the onset of the festive season. Our retail strength index also indicates that rural sentiments remained strong on a YoY basis.”

August, as in July, saw most manufacturers, across segments, rationalise their inventory levels. Hero MotoCorp, dispatched 358,616 units to its showrooms across India, 10,003 units more than it did in August 2023. This gives it an overall two-wheeler market share of 26.80% compared to 27.69% a year ago. There is an intense battle currently underway between Hero and arch rival Honda Motorcycle & Scooter India (HMSI).

In August, the retail sales difference between Hero MotoCorp and HMSI has shrunk to just a little over 6,000 units. HMSI dispatched 352,605 units in August, 41,579 additional units than it did in August 2023 – this sees its market share grow to 26.35% from 24.70% and just 0.45% behind Hero MotoCorp. Though Hero remains ahead of HMSI in cumulative sales, the months ahead will witness a continuation of the exciting battle for market leadership, what with the sales gap reducing with every month.

TVS Motor Co, the No. 3 OEM, sold 236,597 units last month – 11,021 units more YoY – which gives it a market share of 17.68%, marginally down on the year-ago 17.92 percent share. In August 2024, TVS sold 17,541 iQube electric scooters, up 13%, which makes for an EV penetration level of 7.41% and a 20% share of India’s e-two-wheeler market which saw sales of 88,471 units.

Bajaj Auto, with sales of 149,031 units, is ranked fourth and has an August market share of 11.14%, down from 11.80% a year ago. The company, which is seeing strong demand for its Chetak EV, particularly after the launch of its affordable model, sold 16,699 units of the e-scooter and sees an EV penetration level of 11 percent. Just like Hero and Honda, Bajaj and TVS are battling for leadership in the EV stakes.

OEM No. 5 is Suzuki Motorcycle India with 79,307 units, an increase of 9,815 units YoY and a market share of 6% versus 5.52% a year ago.

Royal Enfield, which sold 54,810 bikes, 4,802 fewer bikes than it did in August 2023, sees its two-wheeler market share reduce to 4.10% from 4.73% a year ago.

3-WHEELERS: 105,478 units, up 1.63% YoY, down 4.54% MoM

3-WHEELERS: 105,478 units, up 1.63% YoY, down 4.54% MoM

Bajaj Auto maintains stranglehold with 36% market share, EVs give it a new charge

he three-wheeler segment, with 105,478 units, registered 1.63% YoY growth but was down 4.54% on July 2024’s 103,782 units. The sector continues to benefit from the surging demand for electric models, which now account for every second three-wheeler sold in the country.

August 2024 sales are the second highest in the year to date after July (110,497), January (97,675), February (94,918), March (105,222), April (80,105), May (98,265) and June (94,321). Bajaj Auto, with 37,760 units maintains its strong grip on the 3W market with a 36% share. The company, which entered the electric 3W market only 15 months ago took No. 2 rank on the EV ladder-board in August.

Piaggio Vehicles sold 7,378 units – 970 fewer than in August 2023 – comprising a mix of diesel, CNG and electric powertrains. This gives it a market share of 7%, down from the 8% it had a year ago.

Mahindra Last Mile Mobility, the leader in the e-3W market, sold a total of 5,740 units across multiple powertrains. This total is 390 fewer units than a year ago and gives MLMM a market share of 5.44%, down from the 5.91% in August 2023.

The OEM table above reveals a number of electric three-wheeler makers, all of which are among the Top 30 e-three-wheeler OEMs in August and January-2024.

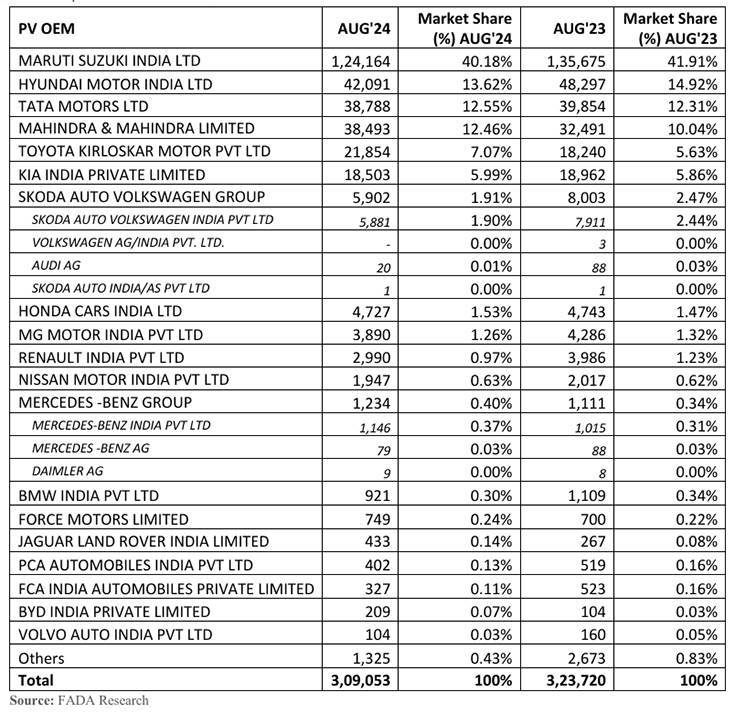

PASSENGER VEHICLES: 309,053 units, down 4.53% YoY, down 4.53% MoM

FADA cautions about high inventory levels with stock days ranging between 70-75 days – 780,000 vehicles valued at Rs 77,800 crore

FADA has red-flagged the passenger vehicle industry as PV sales fell by 3.46% MoM to 309,053 units and 4.53% YoY. Even with the arrival of the festive season, the market remains under significant strain due to delayed customer purchases, poor consumer sentiment and persistent heavy rains.

According to FADA president Manish Raj Singhania, “Inventory levels have reached alarming levels, with stock days now stretching to 70-75 days and inventory totalling 780,000 vehicles, valued at an alarming Rs 77,800 crore. Rather than responding to the situation, PV OEMs continue to increase dispatches to dealers on a MoM basis, further exacerbating the issue.”

He added, “FADA urgently calls upon all banks and NBFCs to intervene and immediately control funding to dealers with excessive inventory. Dealers must also act swiftly to stop taking on additional stock to protect their financial health. OEMs, too, must recalibrate their supply strategies without delay, or the industry faces a potential crisis from this inventory overload. If this aggressive push of excess stock continues unchecked, the auto retail ecosystem could face severe disruption.”

Market leader Maruti Suzuki sold 124,164 units last month – 11,511 fewer units than a year ago – and 5,013 units less than July 2024’s 129,177 units. Its market share is down to 40% from 42% a year ago. Hyundai Motor India sold 42,091 units and sees its share drop to 13.62% from 14.92% a year ago. Tata Motors, with 38,788 units, is just 295 units ahead of Mahindra & Mahindra while Toyota Kirloskar Motor, which is witnessing a strong run of demand for its portfolio of cars, SUVs and MPVs, sold 21,854 units to see its PV share increase to 7% from 5.63% a year ago. Kia India, with 18,503 units, has also gained in market share.

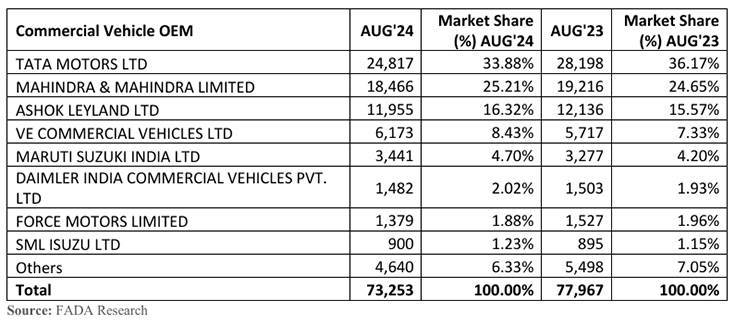

COMMERCIAL VEHICLES: 73,253 units, down 6% YoY, down 8.50% MoM

COMMERCIAL VEHICLES: 73,253 units, down 6% YoY, down 8.50% MoM

CV segment continues to struggle amid multiple challenges

Commercial vehicle sales experienced a sharp drop, with an 8.5% MoM decline and a 6.05% YoY fall to 73,253 units. According to FADA, CV OEMs “have pointed to key challenges such as heavy rains, floods and landslides, which have severely impacted market activity. Additionally, reduced construction activity and sluggish demand in industrial sectors have further strained sales. The CV segment continues to struggle, facing pressure from steep discounting by competitors, which has only intensified the decline. Weak sentiment, coupled with inventory and cash flow challenges, continues to affect the industry overall.”

FADA’s near-term outlook: cautiously optimistic

Even as the festive season begins with Ganesh Chaturthi on September 7, there are several challenges that could impact auto sales in the near term. FADA’s near-term commentary states that with additional rainfall forecast for September by IMD, there is a significant risk to crops nearing harvest, particularly those planted in late June with a 75 to 90-days maturity cycle. Continued heavy rains could negatively affect rural sales, as reduced agricultural output may lead to diminished purchasing power.

Additionally, the Shraddh period in September, regarded as an inauspicious time for purchases, is expected to pause sales for some time. In the CV segment, sluggish construction activity, liquidity issues and weather-related disruptions are likely to suppress demand further. Aggressive discounting practices continue to pressure dealers, leading to reduced profitability and a generally cautious market sentiment.

On the positive side, the upcoming festivals, such as Ganesh Chaturthi, Onam and Navratri, are expected to boost consumer sentiment, especially in urban areas. Moreover, favourable rainfall in certain regions has improved agricultural prospects, which could enhance purchasing power in rural areas as the monsoon subsides. In the CV segment, increasing demand for iron ore, steel transport, and tippers offers a potential lift, supported by new model launches and marketing efforts from OEMs.

Given these factors, FADA remains cautiously optimistic about the near-term outlook. While the festive season and improved rural demand present promising opportunities for growth, ongoing weather uncertainties and high inventory levels may temper the overall recovery. To navigate these challenges, strategic inventory management and targeted marketing initiatives will be crucial in maximizing festive sales and mitigating risks from adverse weather conditions.