Of the total estimated wholesales of 3.53 million passenger vehicles in the past 10 months of FY2025, up 2% YoY (April 2023-January 2024: 34,76,319 units), the share of passenger cars is now down to 31% compared to 37% a year ago.

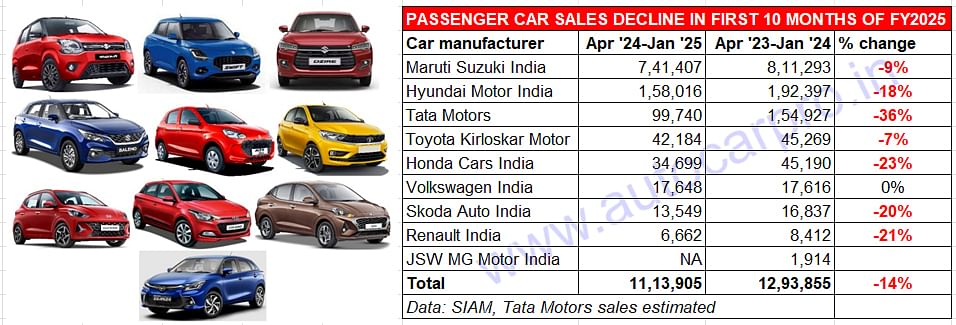

In the first 10 months of FY2025, an estimated 11,13,905 cars have been sold, down 14% on year-ago dispatches of 12,93,855 units. Year on year, 179,950 fewer hatchbacks and sedans have been sold and this is reflected in the sales numbers of all the OEMs in this segment. In FY2024, total passenger car sales were 1.54 million units (15,48,943 units, down 11.4% YoY). With two months left to go in FY2025, the difference is a yawning 435,038 units.

PLENTY OF RED INK IN PASSENGER CAR SALES STATS

A look at the carmakers’ wholesales stats for the past 10 months shows plenty of red ink. Maruti Suzuki India has sold 69,886 fewer cars than it did a year ago: the 741,407 units are down 9%. The decline is across all its three vehicle categories.

Hyundai Motor India, which sells two hatchbacks (Grand i10 Nios, i20) and two sedans (Aura, Verna), has sold 158,016 units, down 18% YoY, and No. 3 carmaker Tata Motors’ sales are down 36% at an estimated 99,740 units.

Toyota Kirloskar Motor, with 42,184 units, is down 7% – the Glanza (40,742 units) accounted for 96% of those sales. Honda Cars India sold 34,669 units comprising the Amaze (25,857 units, -15%) and City (8,842 units, down 39%).

Volkswagen India’s wholesales are flat at 17,648 units of the Virtus sedan (up 0.18%). Skoda Auto sold 13,549 units, down 20% YoY. The Skoda Slavia, which sold 13,501 units, is down 19% YoY. Renault India sold 6,662 Kwids, down 21% YoY. Sales stats of the MG Comet EV are not available with SIAM.

UTILITY VEHICLES DRIVE CLOSER TO FY2024’S RECORD 2.52 MILLION SALES

UTILITY VEHICLES DRIVE CLOSER TO FY2024’S RECORD 2.52 MILLION SALES

Conversely, what is the passenger car segment’s loss is the utility vehicle (SUV and MPV) segment’s gain: a 6% share. As per SIAM and estimated wholesales for the April 2024 to January 2025, the UV segment has clocked total sales of 22,99,466 units, up 12% YoY (April 2023 to January 2024: 20,61,073 units).

This translates into 238,393 additional UVs sold YoY, as a result of which the UV share of the PV segment has risen to 65% from 59% a year ago. In FY2024, the UV segment hit record sales of 25,20,691 units (up 25.8% YoY) and had a 59% share of the record 4.21 million PVs sold last fiscal. Now, with February and March left to go in FY2025, the UV segment is 221,225 units away from that number.

In terms of 16 OEM UV sales, Maruti Suzuki leads the charge with 594,056 units, up 14% YoY. Four Maruti models – Ertiga (159,302 units), Brezza (157,225 units), Fronx (131,086 units) and Grand Vitara (102,859 units) – account for 550,472 units or 92% of that number. Mahindra & Mahindra has sold 453,019 UVs in the past 10 months – an additional 76,187 units YoY – to register 20% growth. M&M’s best-selling models are the Scorpio twins (137,311 units), XUV 3XO (85,990 units), XUV 700 (78,763 units), Bolero (78,029 units) and the Thar / Thar Roxx (66,650 units).

Tata Motors has dispatched an estimated 355,794 SUVs in the first 10 months of FY2025, up 13%. These wholesales comprise the Punch (164,294 units), Nexon (131,374 units), Currv (26,751 units), Safari (17,058 units) and the Safari (16,317 units).

Hyundai Motor India, ranked fourth on the UV table, dispatched 341,103 UVs. The top three models are the Creta / Creta Electric (160,495 units), Venue (98,547 units) and the Exter (66,150 units).

Toyota Kirloskar Motor, which has registered wholesales of 212,363 units, has seen a YoY increase of 40 percent. TKM’s bestsellers are the Innova Crysta / Hycross and the Hyryder.

Kia India, the last of the UV OEMs with over 200,000 sales, has dispatched 204,656 units comprising the Sonet (84,502 units), Seltos (59,647 units), Carens (53,779 units), Syros (5,546 units), Carnival (892 units) and the EV 6 (290 units).

ALSO READ: Top 10 cars in first 10 months of FY2025